Earnings, Inflation & Housing Shape Markets

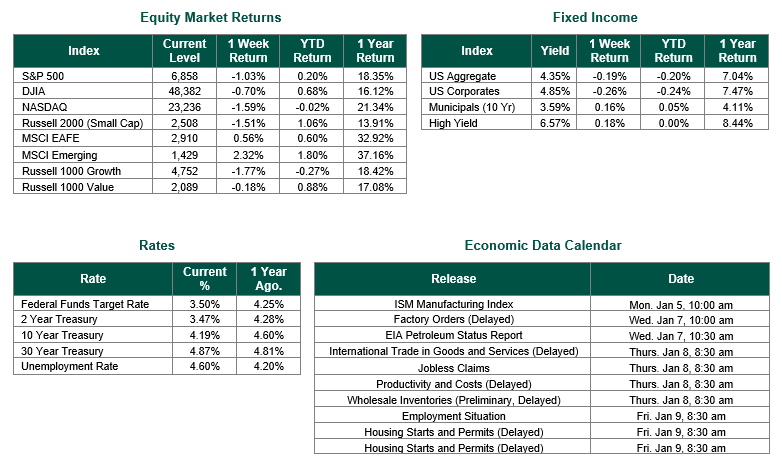

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 6940, representing a decrease of 0.36%, while the Russell Midcap Index moved +0.71% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 2.05% over the week. As developed international equity performance and emerging markets were positive, returning 0.38% and 1.41%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.22%.

Last week, U.S. equities showed varied responses as the fourth-quarter earnings season began. Major banks delivered uneven results. For example, JPMorgan Chase and Citigroup shares fell after reporting lower quarterly profits, influenced in part by one-time charges and sector pressures. In contrast, Morgan Stanley and Goldman Sachs shares advanced, driven by stronger-than-expected investment banking and trading revenue. Shifting to the Technology sector, Taiwan Semiconductor’s fourth-quarter results, released on January 15, featured a substantial profit increase and positive guidance tied to artificial intelligence (AI) demand, which bolstered investor sentiment overall.

The Bureau of Labor Statistics reported the December core CPI on January 13, rising 0.2% month-over-month and 2.6% year-over-year—the lowest annual rate for this inflation gauge since March 2021—below expectations of 0.3% and 2.7%. Headline CPI increased 0.3% month-over-month and 2.7% year-over-year. November retail sales grew 0.6%, exceeding forecasts of about 0.4% and recovering from October’s dip. The delayed November PPI showed a 0.2% month-over-month rise and a 3.0% year-over-year increase, up from prior readings, largely due to energy costs.

October’s new single-family home sales reached a seasonally adjusted annual rate of 737,000, above estimates of roughly 725,000. December existing home sales rose 5.1% to 4.35 million (seasonally adjusted annual rate), surpassing projections of around 4.18 million, supported by lower mortgage rates and moderated price appreciation. The 30-year fixed mortgage rate also neared 6% by week’s end, per Freddie Mac.

These developments illustrate a market environment shaped by corporate results, moderating inflation, and resilient consumer/housing activity amid policy uncertainties. Given the significant impact of these readings on the market and the economy, we believe it’s prudent to work with investment professionals to ensure your portfolio remains consistent with your goals, risk tolerance, and investment timeframe as we navigate a new year that will likely be filled with more volatility and uncertainty than the previous year.

Best wishes for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 1/16/26. Earnings data sourced from Fact Set on 1/13/26 and 1/15/26. CPI and PPI sourced from the BLS on 1/13/26 and 1/14/26, respectively. Retail sales from the US Census Bureau on 1/14/26. Home Sales sourced from the US Department of Housing and Urban Development on 1/13/26. Calendar Data from Econoday as of 1/20/26. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.

{kind=link}