Geopolitics and Inflation Cause Market Volatility

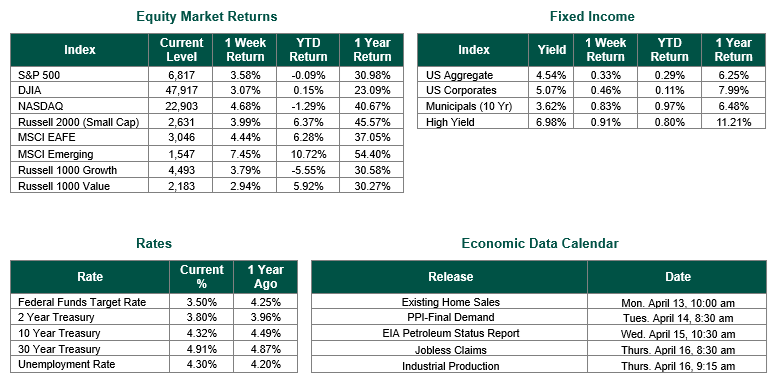

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 6817, representing an increase of 3.58%, while the Russell Midcap Index moved +1.89% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned +3.99% over the week. As developed international equity performance and emerging markets were positive, returning 4.44% and 7.45%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 4.32%.

Market performance last week was shaped by a mix of softer domestic data, sticky inflation, and shifting geopolitical risk, with the Iran conflict and oil prices dominating the macro narrative. Durable goods orders for February fell 1.4%, well below the 0.4% increase expected, after a revised 0.5% decline in January, signaling softer capital spending and industrial demand. The Fed’s March 17–18 meeting minutes, released that week, reinforced a cautious policy stance, with officials still focused on inflation risks and not signaling any rush to ease. The third estimate for Q4 2025 gross domestic product (GDP) showed the economy growing at a 0.5% annualized rate, down from the prior 0.7% estimate, indicating slower-than-previously-thought momentum. Personal income for February slipped 0.1% versus expectations for a 0.3% gain, while personal spending rose 0.5% as expected, with real spending up only 0.1%, suggesting consumers were still active but feeling some strain. Weekly jobless claims rose to 219,000, a bit above the roughly 210,000 forecast and higher than the prior week’s revised 203,000, but still consistent with a relatively healthy labor market. The widely watched CPI inflation gauge for March came in at 0.9% month over month and 3.3% year over year, matching the monthly estimate but remaining hotter than February’s 0.3% monthly and 2.4% annual pace. Consumer sentiment was the week’s weakest economic data point, with the University of Michigan’s preliminary April reading dropping to 47.6 from 53.3 in March and falling short of expectations near 51.5, underscoring growing household pessimism about inflation and the outlook.

Geopolitically, investor focus stayed fixed on the ongoing turmoil in the Middle East, where developments around the Iran conflict and the Strait of Hormuz drove big moves in oil and risk assets. Early in the week, signs of possible de-escalation helped equities rebound and pushed energy prices lower. However, the market still had to digest the reality that the conflict had already lifted gasoline and other energy-linked prices, feeding directly into the March CPI report. By the end of the week, the message to markets was clear: relief rallies could appear on the back of ceasefire headlines, but the broader tone remained fragile because inflation risk and geopolitical uncertainty were still overriding the usual playbook. Our thoughts remain focused on the brave men and women of the U.S. Military and our allies during this conflict in the Middle East.

Best wishes to all for the week ahead.

Equity and Fixed Income Index returns sourced from Bloomberg on 4/10/26. PMI data are sourced from S&P Global. Durable goods data are sourced from the U.S. Census Bureau. FOMC Minutes are sourced from the Federal Reserve. GDP and Personal income data are sourced from the U.S. Bureau of Economic Analysis. Weekly Jobless Claims are sourced from the U.S. Department of Labor. CPI data are sourced from the U.S. Bureau of Labor Statistics. Consumer Sentiment data are sourced from the University of Michigan. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.