A Hawkish Pause?

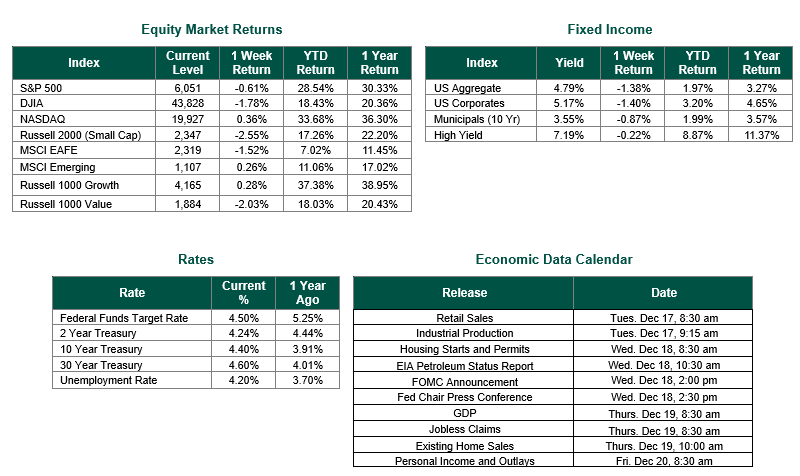

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 6051, representing a decrease of 0.61%, while the Russell Midcap Index fell 2.33% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, declined 2.55% over the week. As developed international equity performance and emerging markets were mixed, returning -1.52% and 0.26%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.40%.

The past week was marked by a mixed bag of economic data, with inflation remaining stubbornly persistent. While the headline CPI reading came in line with expectations at 2.7% on an annual basis, core inflation remained elevated, driven primarily by shelter costs. This reading suggests that the Federal Reserve (Fed) may need to maintain a hawkish stance with respect to interest rates for longer than initially anticipated.

Last week’s surprise increase in initial jobless claims added to concerns about a potential slowdown in the labor market. Although some seasonal factors may have contributed to this rise, the trend of increasing continuing claims remains worrisome.

Despite these developments, market expectations for a rate cut at the upcoming Federal Open Market Committee (FOMC) meeting this meeting have solidified. However, given the recent inflation data, the Fed may opt for a “hawkish pause,” maintaining rates at their current level while signaling future rate hikes if necessary. However, the outlook for rate cuts next year will likely remain intact. As a result, we would not be entirely surprised if the Fed paused following their final meeting of the year and then adopted a more gradual pace of interest rate cuts moving forward.

In the fixed income market, rising U.S. Treasury yields weighed on both Treasuries and investment-grade corporate bonds. High-yield bonds, on the other hand, experienced increased trading activity following the CPI (Consumer Price Index) report but subsequently declined due to broader market sentiment and rising yields.

As we head into the Fed’s big decision this week, investors should remain vigilant and closely monitor economic indicators and central bank policy announcements. A thoughtful approach, coupled with a diversified portfolio, is recommended to help navigate the current market environment.

Best wishes for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 12/13/24. Economic Calendar Data from Econoday as of 12/16/24. CPI data is sourced from the Bureau of Labor Statistics on 12/11/24. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.