Does Recent Jobs Data Lend to Another Rate Cut?

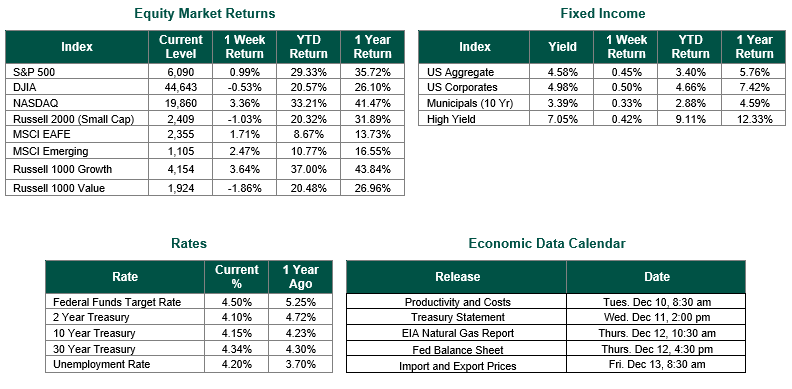

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 6090, representing an increase of 0.99%, while the Russell Midcap Index moved -0.72% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -1.03% over the week. As developed international equity performance and emerging markets were higher, returning 1.71% and 2.47%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 4.15%.

New employment reports were plentiful in last week’s news cycle. Investors were presented with data from the JOLTS report for October, the ADP Employment report for November, the weekly Jobless Claims for the week of November 30th and the November Employment situation report. Away from employment data, investors were also reviewing consumer sentiment for November and a great deal of commentary from Fed Reserve officials.

The Labor Department’s November JOLTS report showed employment listings nudged lower to 8.79 million, about in line with the consensus estimate for 8.8 million and the lowest since March 2021. Openings fell by 62,000, though the rate of vacancies as a measure of employment was unchanged at 5.3%. The ADP National Employment Report reported that private sector employment increased by 146,000 jobs in November and annual pay was up 4.8 percent year-over-year. Jobless claims for the week of November 30th were 224,000, slightly higher than both the consensus estimate (215,000) and the prior week’s revised total (215,000).

On Friday, the Labor Department reported that the US economy added 227,000 jobs in November. A stronger showing than October’s revised total of 36,000. That sharply lower tally for October was partly due to striking workers at Boeing and two major hurricanes that prevented the Bureau of Labor Statistics from gathering data in parts of the Southeast. The November unemployment rate ticked up to 4.2% from 4.1%, marking the first time since 2021 that it has been at or above 4% for six consecutive months.

According to data released on Friday, consumer sentiment, as measured by the University of Michigan’s Consumer Sentiment Index, rose to 74.0, marking a fifth consecutive month of increase and representing the highest reading in several months.

Federal Reserve Chair Jerome Powell on Wednesday said the economy is stronger now than the central bank had expected in September when it began reducing interest rates. “The U.S. economy is in very good shape and there’s no reason for that not to continue …the downside risks appear to be less in the labor market, growth is definitely stronger than we thought, and inflation has come in a little higher,” Powell said at a New York Times event. “So the good news is that we can afford to be a little more cautious as we try to find neutral.”

In-depth comments by some of Powell’s key colleagues this week have pointed in the direction of a third straight interest-rate cut, with Governor Christopher Waller stating on Monday that he was “Leaning towards” a reduction even as others decline to pre-commit to that outcome.

Best wishes for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 12/6/24. All Employment data is sourced from The Labor Department. Consumer Sentiment is sourced from the University of Michigan. Comments from Federal Reserve Officers were sourced from the Federal Reserve. Economic Calendar Data from Econoday as of 12/6/24. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.