Last Week’s Markets in Review: Fed Stays Aggressive and Markets Tumble

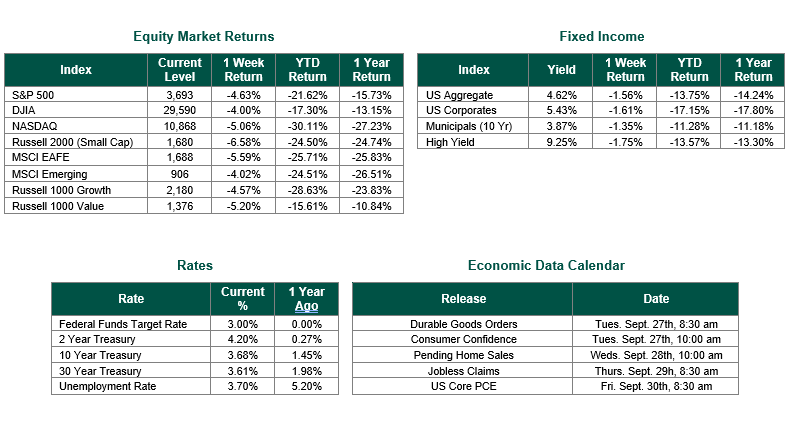

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index closed the week at a level of 3,693, representing a decrease of 4.63%, while the Russell Midcap Index moved -5.88% lower last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -6.58% over the week. As developed, international equity performance and emerging markets were lower returning -5.59% and -4.02%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 3.68%.

The greatly anticipated Federal Reserve meeting for September occurred this past week. Regular readers of prior Capital Markets Updates are very aware that we have been focused on monetary policy. In these updates, we have shared with readers both market sentiment around future interest rate hikes and our own interest rate thesis. Like most market participants, we have reported and analyzed the probability of this interest rate hike leading up to the announcement. The announced rate hike matched market expectations. In the days prior to the Fed’s meeting, the probability of a 75 Bp (0.75%) hike was over 95%. Even though the rate increase was in line with the expectations, markets exhibited great volatility after the rate announcement. For example, U.S. Treasury yields increased to levels not seen in a decade and equities retreated to the previous 2022 lows reached in June. We will discuss what we believe are the reasons for this market volatility throughout the remainder of this update.

It is our belief that the violent movements in the markets are centered around the changes in the Fed’s “Dot Plot” chart from the June meeting (see both charts below). We also believe that Chairman Powell’s willingness to accept the “R” word (Recession) as a necessary outcome to tame inflation has caused the spike in rates and the declines in equities.

Generally, the “Dots” all moved higher from June. The September version of the chart made market participants aware that committee members expect that they will remain aggressive for a prolonged period of time. With the majority of 2022 “Dots” falling between 4.0% and 4.5%, market participants had to accept that there could be two additional 75 Bps moves prior to the end of 2022. Regarding 2023, the June chart showed a range from 2.75% to 4.50%, and only one FOMC member was at the high end of the range. The majority of FOMC members held the opinion that Fed Funds rate would not exceed 4.0%. The September 2023 “Dots” revealed that the members now believe that they will be forced to move the Fed Funds Target Rate higher and keep it elevated for a longer period. All committee members, apart from one, currently project a Fed Funds rate ranging from 4.25% to 5.0% for 2023.

Fed Chair Powell held a press conference immediately after the Fed’s announcement last week. During this press conference, Powell made several comments that lead market participants to believe that the Fed is willing to cause a recession as it continues to battle inflation. Powell’s comments included, “No one knows whether this process will lead to a recession” and, “The chances of a soft landing are likely to diminish to the extent that policy needs to be more restrictive, or restrictive for longer. Nonetheless, we’re committed to getting inflation back down to 2%.”

As our readers can observe, the “Dot Plot” is a fluid analytical tool. Fed members will have an opportunity to access a great deal of data prior to their next scheduled meeting on November 2nd and throughout the remainder of 2022. It is quite possible that the already instituted rate hikes will cause inflation to start to decline and the economy to continue to contract. If this does occur, then it is likely that the Fed will become less aggressive in their policy. A less hawkish (though not necessarily dovish) Federal Reserve may serve as a tailwind for stocks as investors will perceive the change as an indication the worst is behind us with respect to the magnitude of interest rate hikes.

Investors should consider all the information discussed within this market update and many other factors when managing their investment portfolios. However, with so much data and so little time to digest, we encourage investors to work with experienced financial professionals to help process all this information to build and manage the asset allocations within their portfolios consistent with their objectives, timeframe, and tolerance for risk.

Best wishes for the week ahead!

The “Dot Plots” for both June and September were sourced from the Federal Reserve’s website. Equity Market and Fixed Income returns are from JP Morgan as of 9/23/22. Rates and Economic Calendar Data from Bloomberg as of 9/23/22. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.