Last Week’s Markets in Review: Fed Talk Leads to More Market Volatility

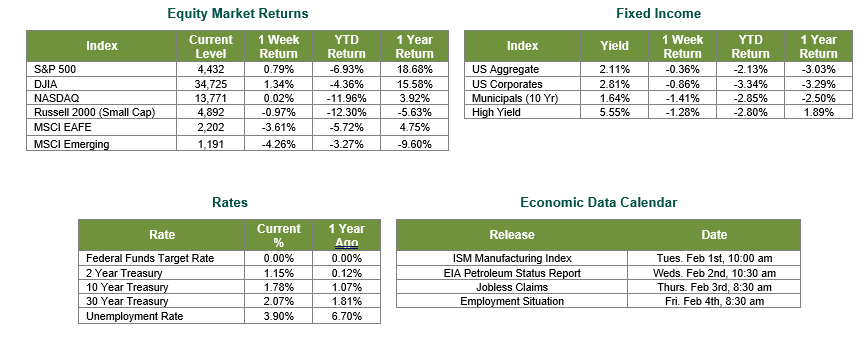

Failed rallies highlighted the week in U.S. equity markets until a breakout on Friday from the S&P 500 Index. The S&P 500 closed the week at a level of 4,432, representing a gain of 0.79%, while the Russell Midcap Index moved 0.31% lower. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -0.97%. International equity performance struggled as developed and emerging markets returned -3.61% and -4.26%, respectively. Finally, the 10-year U.S. Treasury yield moved 3 basis points higher over the week, closing at 1.78% on Friday.

The spotlight last week was on Wednesday’s meeting of the Federal Open Market Committee (“FOMC”). Judging by market activity in 2022 thus far, the writing was on the wall for an earlier interest rate hike “liftoff” than what was previously anticipated after the Federal Reserve’s final meeting of 2021 in December. According to the CME group, the market is now pricing in an 81% chance of a rate hike in March, up from 50% a month ago. So what exactly transpired after the group convened and investors eagerly awaited Chairman Powell’s remarks? Consistent with market expectations, “the Committee expects it will soon be appropriate to raise the target range for the federal funds rate.” With this information, it appears March will be a significant month for policy normalization, with the Fed Funds rate likely moving higher and the ending of asset purchases (i.e., tapering). Remember, there is also the nearly $9 trillion Federal Reserve balance sheet to unwind, which had doubled to support the economy through the pandemic. The combination of all three actions forms the basis of the Fed’s “TNT” (Taper-Narrow-Tighten) program that we have been speaking about for the past couple of months.

While markets have sold off this year due largely to fears of a more aggressive Fed, investors should also appreciate the positive aspects of interest rate hikes by the Federal Reserve. For example, the Fed believes rate moves can be made because “Indicators of economic activity and employment have continued to strengthen.” Consider last week’s 4th Quarter 2021 GDP advance of 6.9%, outpacing expectations of 5.5%. All else equal, and absent extreme adverse events, such as a new material COVID-19 variant, a growing economy should be able to handle a tightening cycle designed to normalize policy and combat high inflation. Historically, a tightening cycle and slowing growth are associated with high volatility and low yet positive returns.

It is also noteworthy that the performance of different investment styles has been uneven thus far in 2022. Large-cap growth stocks have fallen over 11% in the U.S., while large-cap value stocks “only” retreated roughly 3.5% year-to-date. The prospect of increasing rates and the risks associated with high inflation amid uncertain economic conditions caused a drawdown in risk assets, particularly a revaluation of long-duration assets. Even with the swift rotation so far this year, value-oriented stocks are far from being overpriced from a historical perspective and, in our view, remain attractive at this time. The pullback in growth stocks may have also created some attractive entry points for certain companies within certain industries. High-quality growth companies have the potential to support performance in a growing yet slowing economy. Quality companies are typically associated with stable earnings growth, high return on equity (ROE), and a relatively lower level of leverage and can be found across many style classes and industries. In addition, companies that have a track record of operating cash flow, earnings growth, and reasonable valuations within more innovative and cutting-edge areas, including the e-commerce ecosystem, are traditionally growth companies that should benefit from the expansion of those industries and technologies.

We anticipated 2022 would have more bouts of short-term volatility than 2021. However, we do believe markets will move higher overall this year. While the uncertainties of inflation, rising interest rates, COVID-19, Fed policy, and even geopolitical tensions are undoubtedly present, opportunities exist. Working with experienced financial professionals can help investors navigate the complex capital markets to build and manage the asset allocations within their portfolio strategies consistent with their objectives, timeframe, and tolerance for risk.

Best wishes for the week, and year, ahead!

Sources for data in tables: Equity Market and Fixed Income returns are from JP Morgan as of 1/28/22. Rates and Economic Calendar Data from Bloomberg as of 1/28/22. International developed markets measured by the MSCI EAFE Index, emerging markets measured by the MSCI EM Index, U.S. Large Cap defined by the S&P 500. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.

Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against loss.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than the original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market, and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.