Last Week’s Markets in Review: GDP, Jobs and Escalating Russia/Ukraine Tensions

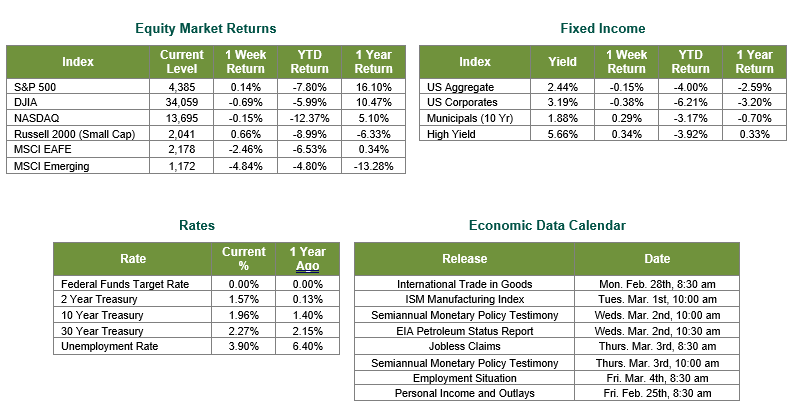

Global equity markets were mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 4,385, representing a gain of 0.14%, while the Russell Midcap Index moved 1.28% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 0.66% over the week. International equity performance was lower as developed and emerging markets returned -2.46% and -4.84%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 1.96%.

Prior to the market open on Thursday, we anticipated the release of GDP and jobless claims data that would help paint a clearer picture towards economic strength, a factor when determining the size of the imminent interest rate hike in March. In a terrifying fashion, these data releases were quickly overshadowed by the unprovoked attack on Ukraine by the Russian military. The attack struck global markets aggressively, as the S&P 500 index dropped 1.50% in the first hour of trading, the MSCI All Country World (ACWI-Ex US) Index fell 3.75% and MSCI Emerging Markets lost 5.14%.

Gross domestic product (GDP) figures in the United States came in line with consensus expectations at 7.0% revised for the 4th quarter and jobless claims reported at 232,000, a noticeable improvement from the 248,000 claims reported for the week prior. However, these data sets were not as relevant to the market as the geopolitical tensions smothering the globe. As investors digested the catastrophic events in Ukraine, markets began reacting inversely. The S&P 500 would end up shooting up 3.03% from its bottom and finish the trading day in positive territory. The market reacted strongly to comments by President Biden with regards to sanctions against Russia and openness to releasing U.S. oil reserves to help combat rising prices. At the same time, investors questioned the future actions of the Federal Reserve and their expected rate hike schedule. Historically, central banks have been reluctant to tighten financial conditions during high-tension geopolitical events due to the levels of uncertainty that surround them. In fact, according to CME Group, the odds of a 50-basis point increase by the Federal Reserve in March declined to just a 17.2% probability.

Any time the world is faced with geopolitical events, global markets face mass heavy amounts of uncertainty. It should be noted, however, that prior to Thursday’s events, equity risk premiums had already risen in anticipation of a Russian invasion along with inflationary and interest rate risks, forcing equities into correction territory, albeit briefly.

On Friday, markets provided positive returns on news that Russia was willing to meet with Ukraine while NATO members would meet separately. Despite the market gains, we are left with uncertainty around the rippling effect on commodities and assets from retaliatory sanctions across the world economy. Regardless of allocations, various assets can, and will, be affected as more information is known on these events. As such, we suggest speaking with financial professionals to determine the potential effects on portfolios and ensure investments are positioned in accordance with objectives, risk tolerance, and time horizon. Our thoughts are with the people of Ukraine as we hope for rapid developments towards peace. Best wishes for the week ahead!

Equity Market and Fixed Income returns are from JP Morgan as of 2/25/22. Rates and Economic Calendar Data from Bloomberg as of 2/25/22. International developed markets measured by the MSCI EAFE Index, emerging markets measured by the MSCI EM Index, U.S. Large Cap defined by the S&P 500. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.

Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against loss.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk, especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than the original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market, and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.