Last Week’s Markets in Review: Hot Inflation Data Moves Markets

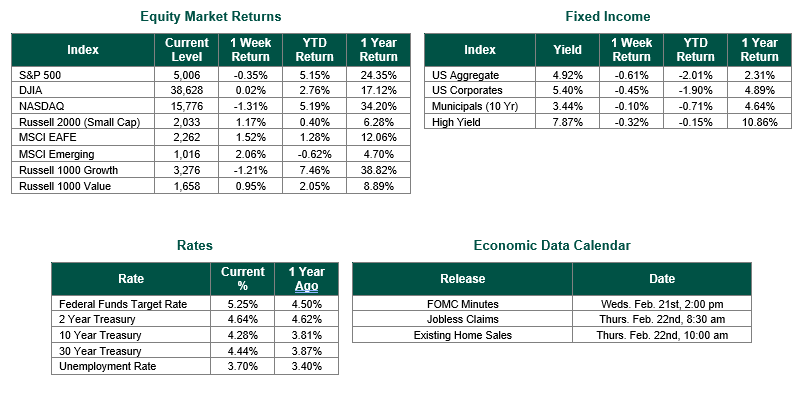

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the Week at a level of 5,006, representing a decrease of 0.35%, while the Russell Midcap Index moved 0.61% last Week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 1.17% over the Week. As developed international equity performance and emerging markets were higher, returning 1.52% and 2.06%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the Week at 4.28%.

Last week two important measures of inflation became available for the market to digest. On Tuesday The Bureau of Labor Statistics released the Consumer Price Index Summary (CPI) for January. The index showed that inflation rose more than expected as stubbornly high shelter prices weighed on consumers. The index rose 0.3% for the month, this was higher than economists surveyed by Dow Jones had expected (0.2%). On a 12-month basis, the index increased by 3.1%, again outpacing expectations of 2.9%. this data created a selloff in equities and an increase in the yield of fixed income instruments.

Later in the week, The Bureau of Labor Statistics also reported the Producer Price Index (PPI) for January. This report also showed inflation at higher levels than the markets expected. PPI, a measure of prices received by producers of domestic goods and services, rose 0.3% for the month, the biggest move since August. The consensus estimate was for an increase of 0.1%. Core PPI, which excludes food and energy, increased 0.5%. This was higher than the consensus estimates of 0.1%.

Away from the inflation data, other economic data for the week included Retail Sales for January. Advance retail sales declined 0.8% for the month, down from a 0.4% gain in December and worse than the estimate for a 0.3% drop.

Overall, the data for the week moved market expectations concerning the timing of the Fed’s first interest rate cut deeper into the current year. Utilizing the CME FedWatch Tool as of February 20th, the first cut will likely occur at the FOMC meeting in July.

Best wishes for the week ahead!

Both CPI and PPI data are sourced from The Bureau of Labor Statistics. Retail Sales data is sourced from the U.S. Department of Commerce. Economic Calendar Data from Econoday as of 2/20/24. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.