Last Week’s Markets in Review: Is More Fiscal Stimulus Needed?

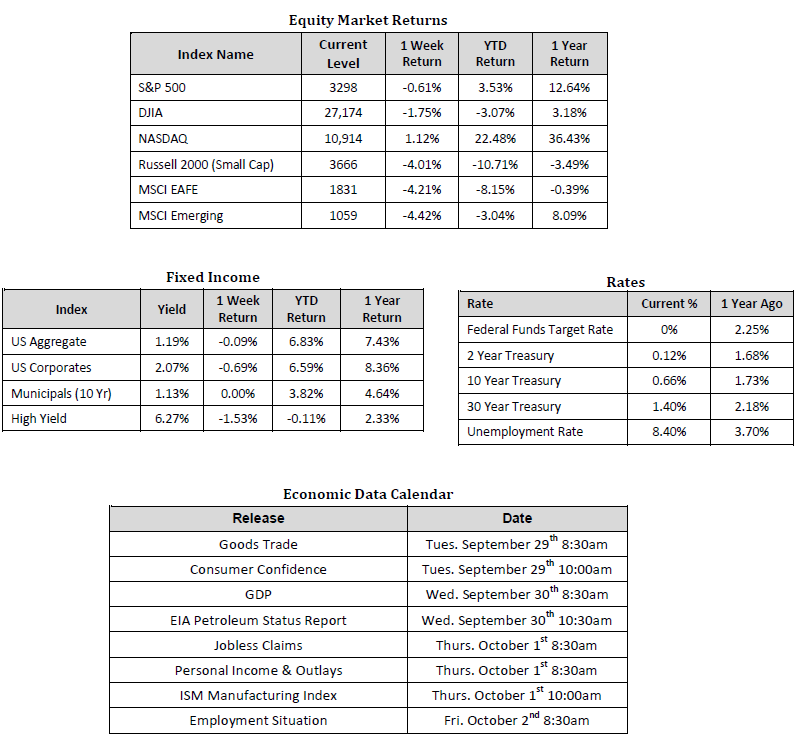

Global equity markets were mixed on the week, with U.S. technology stocks pushing higher, while essentially all other global equity indexes retreated. . In the U.S., the S&P 500 Index fell to a level of 3,298, representing a loss of 0.61%, while the Russell Midcap Index lost 1.48% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, lost 4.01% over the week. Moreover, developed and emerging international markets gave back 4.21% and 4.42%, respectively. Finally, the 10-year U.S. Treasury pulled back to 0.66%, 4 basis points lower than the prior week.

On the economic data front, investors tried to make sense of the divergence between housing market figures that suggest the existence of a robust underlying economy and jobless claims numbers that may cast doubt on the recovery of the labor market. Existing home sales and new home sales registered at 6 million and 1.011 million last week respectively, both clocking in above consensus expectations. Meanwhile, 870,000 additional American’s filed for unemployment benefits.

With consumption accounting for nearly 70% of U.S. Gross Domestic Product (GDP), it’s no secret that the health of the U.S. economy is largely contingent upon the U.S. consumer’s health. As such, it’s imperative to track trends in consumer spending to gain better insight into the vibrancy of the underlying economy. One way we assess the vitality of the consumer is by analyzing trends in retail sales. According to Bloomberg, retail sales track the resale of new and used goods to the general public, for personal or household consumption, and are thus incredibly useful in analyzing month-to-month changes in consumer spending.

A review of the chart below provides a clear indication that retail sales growth has slowed of late, a trend not typically associated with the recovery phase of the economic cycle. A closer look shows retail sales in nearly all categories bottoming out in April, which makes sense given the near entirety of the economy was shut down due to the stay at home orders that were implemented in states across the country. What makes slightly less sense is all categories, except for clothing, and restaurants and bars, recovered so much so that they actually exceeded pre-pandemic levels, all while the unemployment rate held above 10%. So, what led to a major boost in retail sales in June while unemployment held at 10%, and why didn’t retail sales continue to grow at the same pace in August?

The most likely explanation for exceptional growth in June retail sales, as well as the mediocre growth in August retail sales, is related to the impact of the fiscal stimulus package passed by the Federal government. In this regard, it is important to remember that part of the multi-trillion dollar stimulus package created in response to COVID-19 was earmarked for increased unemployment benefits. In fact, those filing for unemployment received an extra $600 on top of the typical assistance, and, in many cases, ended up earning more while unemployed than they did when they were employed. It appears that most American’s took the extra money in their pockets and immediately put it back into the economy, fueling exceptional growth in June retail sales. These enhanced unemployment benefits expired in August, likely explaining the more cautious stance taken by consumers, evidenced by slower growth in August retail sales.

The question now becomes whether we can expect minimal, or even negative, retail sales growth in the months ahead? With millions of Americans still unemployed, the unemployment rate at 8.4%, and service industries (Exs. Clothing/Restaurants) still well below pre-pandemic levels, it seems reasonable to expect continued sluggishness in retail sales. One potential remedy is for America’s congressional leaders to come together and pass a desperately needed follow-up fiscal package, which is exactly what Federal Reserve Chairman Jerome Powell and Treasury Secretary Steve Mnuchin have implored Congress to do for weeks.

The current inability of Congress to pass an additional stimulus package, the on-going debate over filling Ruth Bader-Ginsburg’s former Supreme Court seat, November’s Presidential and Congressional elections, and COVID-19 will all contribute to increased levels of volatility as we move into year-end. For these reasons, we continue to encourage investors to stay disciplined and work with experienced financial professionals to help manage their portfolios through various market cycles within an appropriately diversified framework consistent with their objectives, timeframe, and tolerance for risk.

We recognize that these are very troubling and uncertain times, and we want you to know that we are always here to help in any way we can. Please stay safe and stay well.

Other Data Sources: Equity Market and Fixed Income returns are from JP Morgan as of 9/25/20. Rates and Economic Calendar Data from Bloomberg as of 9/25/20. International developed markets measured by the MSCI EAFE Index, emerging markets measured by the MSCI EM Index, U.S. Large Cap defined by the S&P 500. Sector performance is measured using GICS methodology. S&P 500 sector performance represents total return figures sourced from Bloomberg. Growth of Retail Sales chart was produced by JP Morgan Asset Management.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index.

Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against loss.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than the original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.