Last Week’s Markets in Review: Making a case for Preferred Stocks

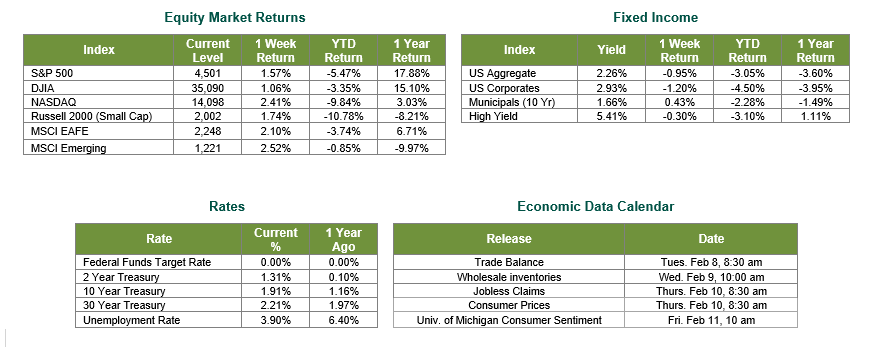

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 4,501, representing a gain of 1.57%, while the Russell Midcap Index moved 2.31% higher last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 1.74% over the week. International equity performance was mixed as developed, and emerging markets returned 2.10% and 2.52%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 1.93%.

We highlighted our “Top 10 Investment Themes for 2022” at the beginning of the year. One of the underlying themes was “Consider Preferreds for Income Potential.” In this week’s update, we will go into greater detail on making a case for preferred stocks based on the current economic and market environment. To avoid being redundant, the basic concept and structure of preferred stocks and general rationale can be found here in the original investment theme article. In making our case for potentially considering preferreds, we will look at two specific characteristics of preferreds that are beneficial based on recent concerns that have been top of the mind of many investors.

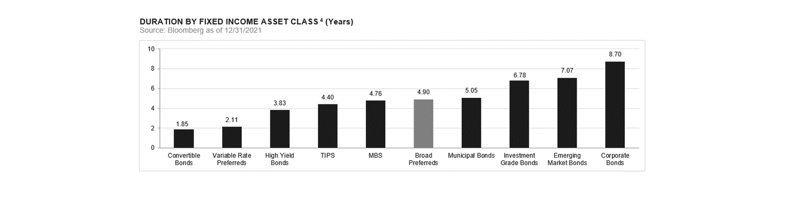

1. Rising interest rates: Interest rates rising is not new news. By now, even the less sophisticated investors have been hearing about interest rates rising throughout the first month of 2022. Regarding rising rates, preferred stocks have characteristics to perform in such an environment as a majority of preferred issues stem from the Financials sector that historically has benefited from higher lending rates. In fact, approximately 54% of the sector weighting between the three largest preferred stock ETFs (Tickers: PFF, PFFD, and PGZ) are allocated towards financials. Additionally, preferred securities typically have shorter durations when compared to other fixed-income assets, which is represented in the chart below. By shortening a portfolio’s duration, investors can potentially help reduce interest rate risk.

2. Inflation: With inflation reaching a 40 year high in December of 2021, many fixed-income investors have been challenged to find attractive sources of income potential as the real return on interest has been drastically devalued. One way to help lessen the blow of inflationary pressures is by investing in higher nominal yields, and preferred securities generally provide just that. For example, the S&P U.S High-Quality Preferred Index currently has an indicated dividend yield of approximately 4.87%, nearly 275 Basis Points (Bp) higher than the U.S. Aggregate Bond Index. In essence, investors achieving higher nominal yields will experience stronger real returns as inflationary environments persist. Real returns can look even more attractive to investors in preferred securities as interest from securities under this umbrella is often treated as qualified dividend income. This form of dividend can help reduce the tax burden from the highest marginal rate of 37% down to a maximum of 23.8%.

As we have shown above, there is certainly a case to be made for preferred securities as a source of income potential in current markets. However, this may not be the case for every investor. For this reason, we believe it is important to speak with financial professionals and determine if these types of securities are appropriate for a given portfolio based on the specified risk tolerance, time horizon, and overall investment objective.

Best wishes for the week ahead!

Equity Market and Fixed Income returns are from JP Morgan as of 2/4/22. Rates and Economic Calendar Data from Bloomberg as of 2/4/22. International developed markets measured by the MSCI EAFE Index, emerging markets measured by the MSCI EM Index, U.S. Large Cap defined by the S&P 500. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.

Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against loss.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than the original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market, and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.