Last Week’s Markets in Review: Manufacturing on the Rebound

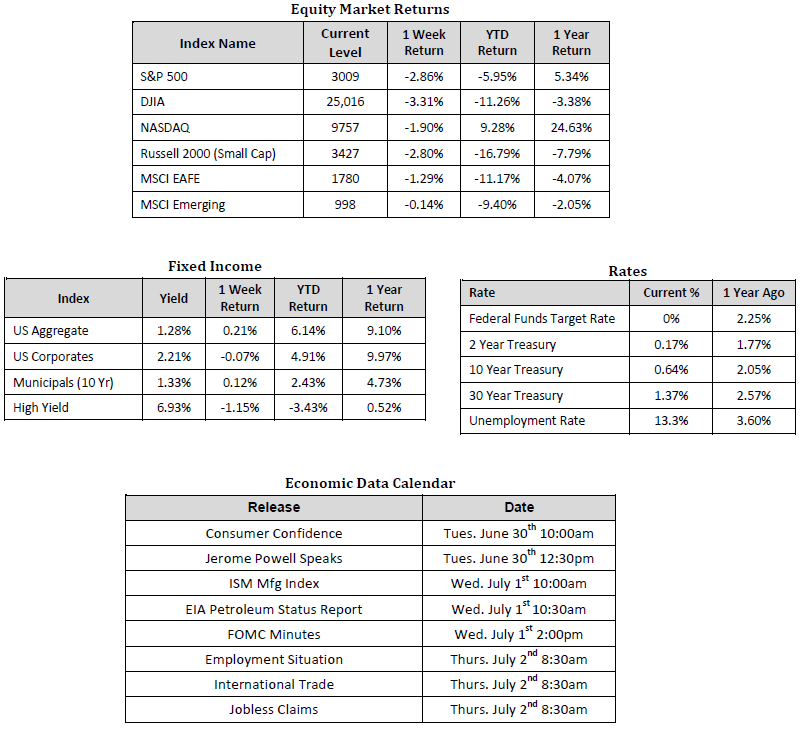

The U.S. equity rally was put on pause last week over concerns of a resurgence in COVID-19 cases in certain geographic areas. In the U.S., the S&P 500 Index fell to a level of 3,009, representing a loss of 2.86%, while the Russell Midcap Index moved 3.31% lower last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -2.80% over the week. International equities fared better than their U.S. counterparts, though still gave up ground, as developed and emerging markets returned -1.29% and -0.14%, respectively. Finally, the yield on the 10-year U.S. Treasury followed suit, finishing the week at 0.64%, down 6 basis points from the week prior.

In this week’s update, we’ll take a look at recent economic data releases. Throughout the COVID-19 pandemic, we’ve discussed how forecasting is an almost impossible exercise in the current market environment. Look no further than our previous market update, which highlighted that the number of companies issuing forward-looking guidance has decreased dramatically. So instead, let’s look at a few key macro indicators to help provide guidance on the likely path of the overall economic recovery.

To start, in recent week’s we’ve seen retail sales surprise significantly to the upside. Recognizing that consumption makes up approximately 70% of U.S. gross domestic product (GDP), this release was certainly encouraging and helped give some credence to the stock market rebound that has taken place since March 23, 2020.

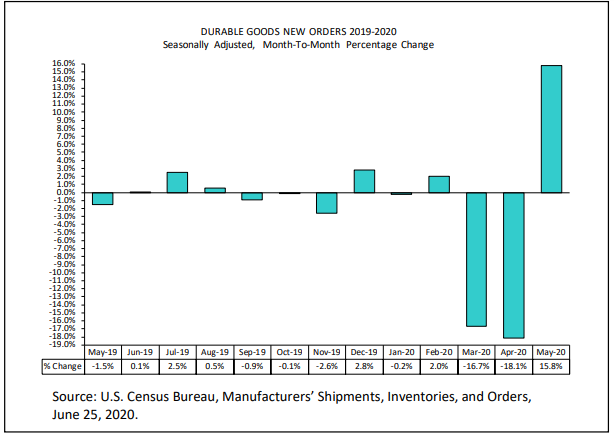

We also received updates on another crucial part of the economic recovery equation…manufacturing. The manufacturing sector is a major component of the economy and an important leading indicator of economic activity that provides insight into the supply chain. Last week, U.S. Services and Manufacturing Flash PMIs both hit 4-month highs. The Flash Purchasing Managers Index (PMI) is a forward-looking estimate of the manufacturing and services sectors and provides an advance reading of the final PMI data. By tracking changes in areas such as output, new orders, and prices, it can help indicate the performance and general direction of the private sector. These readings both came in roughly 10 points higher than the previous month and were just below 50. While the readings didn’t quite make it over the 50-mark, which would indicate improving conditions instead of contractionary territory, they weren’t far off and provide additional support for other recent, generally positive economic data. In addition, and more importantly, durable goods orders surged 15.8% in May. This is compared to estimates which were in the +10% range and also represented the largest month-to-month swing in 6 years, following the decline of 18.1% in April.

It’s easy to glaze over the durable goods orders release as it may not be as mainstream as other readings such as GDP, unemployment, and consumer spending, to name a few. Truthfully, its name, durable goods, may not be very apparent to the average retail investor. However, it is quite important, and last week’s reading was very positive. Durable goods orders are a monthly survey conducted by the U.S. Census Bureau and an indicator of manufacturing activity. Durable goods orders refer to those typically more expensive items that are meant to last three or more years. Examples include industrial machinery, computer equipment, and even cars and planes. It’s also important to review the details of these readings because very costly, and often infrequent orders may skew the data in some months. However, the core goods, which exclude transportation and defense sectors, still increased more than double the median projection, according to Bloomberg. These durable goods orders placed can point to future increased factory activity down the entire supply chain. In addition, consumers and businesses typically are diligent about the purchase of large-ticket items so an increase in these orders can point to increased confidence and a positive outlook.

While many will debate whether these economic data readings are strong enough to support current stock market levels, it’s hard to argue that there are not any signs that the economy is on the rebound. However, we still have a long way to go before getting back to pre-COVID-19 economic growth levels and there will undoubtedly be bouts of heightened stock market volatility along the way as news on the virus itself continues to unfold. An experienced financial professional can help manage portfolios through various market cycles within an appropriately diversified framework that is consistent with investor’s objectives, time-frame, and tolerance for risk.

We recognize that these are very troubling and uncertain times and we want you to know that we are always here for you to help in any way that we can. Please stay safe and stay well.

Sources for data in tables: Equity Market and Fixed Income returns are from JP Morgan as of 6/27/20.

Rates and Economic Calendar Data from Bloomberg as of 6/27/20. International developed markets measured by the MSCI EAFE Index, emerging markets measured by the MSCI EM Index, U.S. Large Cap defined by the S&P 500. Sector performance is measured using GICS methodology.

Important Information and Disclaimers

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against loss. Hennion & Walsh is the sponsor of SmartTrust® Unit Investment Trusts (UITs). For more information on SmartTrust® UITs, please visit www.smarttrustuit.com. The overview above is for informational purposes and is not an offer to sell or a solicitation of an offer to buy any SmartTrust® UITs. Investors should consider the Trust’s investment objective, risks, charges and expenses carefully before investing. The prospectus contains this and other information relevant to an investment in the Trust and investors should read the prospectus carefully before they invest.

Investing in foreign securities presents certain risks not associated with domestic investments, such as currency fluctuation, political and economic instability, and different accounting standards. This may result in greater share price volatility. These risks are heightened in emerging markets.

There are special risks associated with an investment in real estate, including credit risk, interest rate fluctuations and the impact of varied economic conditions. Distributions from REIT investments are taxed at the owner’s tax bracket.

The prices of small company and mid-cap stocks are generally more volatile than large company stocks. They often involve higher risks because smaller companies may lack the management expertise, financial resources, product diversification and competitive strengths to endure adverse economic conditions.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than the original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market, and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.