Markets Thankful for November

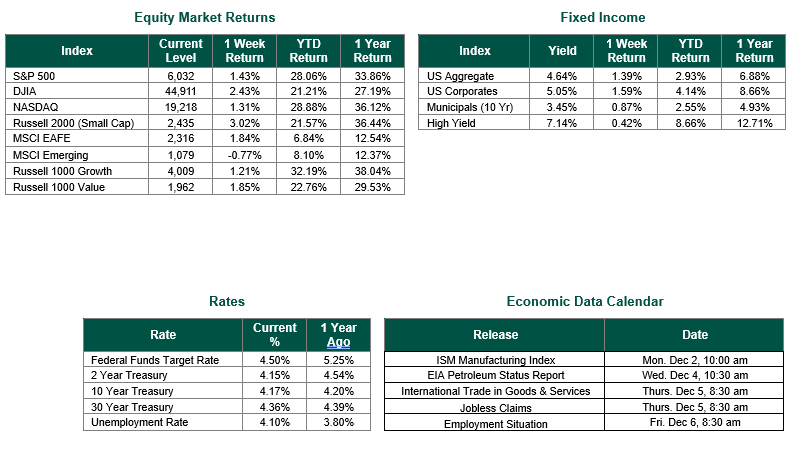

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 6032, representing an increase of 1.43%, while the Russell Midcap Index moved 0.93% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 3.02% over the week. As developed international equity performance and emerging markets were mixed, returning 1.84% and -0.77%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 4.17%.

Equity markets capped off the month of November with the best monthly performance of 2024. Stocks continued their upward trajectory last week, with the Dow Jones Industrial Average, S&P 500 Index, and S&P 400 MidCap Index reaching new intraday highs. The small-cap Russell 2000 Index even surpassed its previous record high. Despite the fact that markets were closed on Thanksgiving Day, trading remained active leading up to the holiday, providing equities the strongest monthly performance of 2024.

Domestic policy and geopolitical factors played a significant role in market sentiment. The nomination of Scott Bessent as Treasury Secretary was well-received by investors. Bessent’s Wall Street experience and focus on economic stability and inflation control alleviated concerns about potential policy extremes.

The recent trend of declining inflation has prompted major central banks to ease monetary policy. This shift is expected to positively impact economic growth, job markets, and corporate profits. Last week’s economic data further solidified this trend. The U.S. economy maintained its momentum, with third-quarter GDP growth revised upward to 2.8%. Additionally, the core Personal Consumption Expenditure (PCE) price index, a key inflation gauge, rose slightly to 2.8% year-over-year, aligning with expectations. While some inflationary pressures, particularly in housing and rent, remain elevated, overall, the inflation picture is improving.

The fixed income market has also shown signs of improvement. After a challenging period marked by rising interest rates, bonds have begun to recover. Investment-grade bonds, in particular, have outperformed cash-like investments over the past 12 months, despite recent yield increases. Lower-quality bonds, with their higher interest rates and relatively stable credit spreads, have been the top performers within the fixed income asset class, emphasizing the importance of diversification.

Best wishes for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 11/29/24. GDP and PCE Data sourced from the Bureau of Economic Analysis on 11/27/24. Economic Calendar Data from Econoday as of 12/2/24. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.