Post-Election Rally Stalls

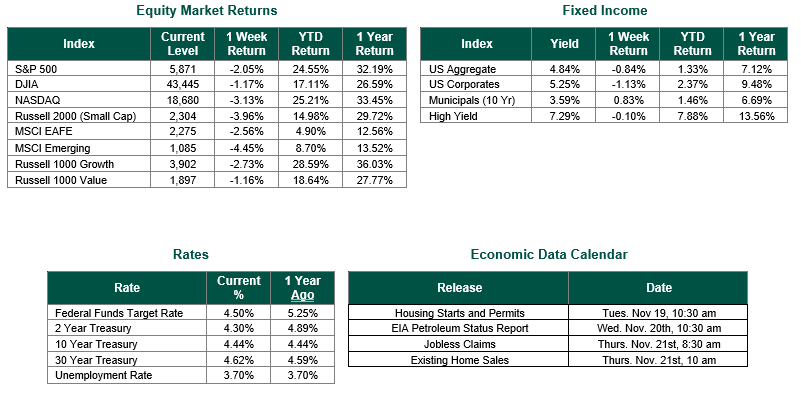

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index closed the week at a level of 5871, representing a decline of 2.05%, while the Russell Midcap Index moved -2.55% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -3.96% over the week. As developed international equity performance and emerging markets were lower, returning -2.56% and -4.45%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.45%.

Equity markets reversed course last week after a strong post-election run and an additional interest rate cut by the Federal Reserve the week prior. All three major U.S. benchmarks retreated following hawkish-leaning comments by Fed Chair Jerome Powell, stating that the central bank is not in a hurry to cut rates given stronger-than-expected economic growth and a stable labor market.

Inflation remained a significant concern last week as both U.S. Consumer Price Index (CPI) and Producer Price Index (PPI) data for October were released. While headline inflation was in line with expectations, underlying inflationary pressures, particularly in services, persisted. Headline CPI rose to 2.6% year-over-year, up from 2.4% in the previous month. Core CPI, which excludes volatile food and energy prices, held steady at 3.3%. Although some components, such as energy, gasoline, certain food items, and new vehicle prices, moderated, others, including housing, rent, and motor vehicle insurance, continued to rise.

In what will be a quiet week for economic releases, investors will likely be hyper-focused on the earnings of tech giant Nvidia (Ticker: NVDA) this Wednesday, November 20. Nvidia is now the world’s largest company by market capitalization and is held by many investors directly or indirectly. As a result, earnings from Nvidia will be closely dissected by the markets to help navigate the explosive growth of the AI revolution, which has led to high current valuations and expectations for several of the companies associated with the AI theme. Shares of Nvidia fell nearly 2% last Friday, with another ~2% fall in pre-market trading as of the time of this writing due to apparent concerns with its Blackwell AI chip experiencing overheating issues in certain servers.

Best wishes for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 11/15/24. CPI and PPI data sourced from the Bureau of Labor Statistics Unemployment data sourced from the Bureau of Labor Statistics on 11/13/2024 and 11/14/2024, respectively. Economic Calendar Data from Econoday as of 11/18/24. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.