Last Week’s Markets in Review: Should Investors Worry about Higher Interest Rate Sensitivity?

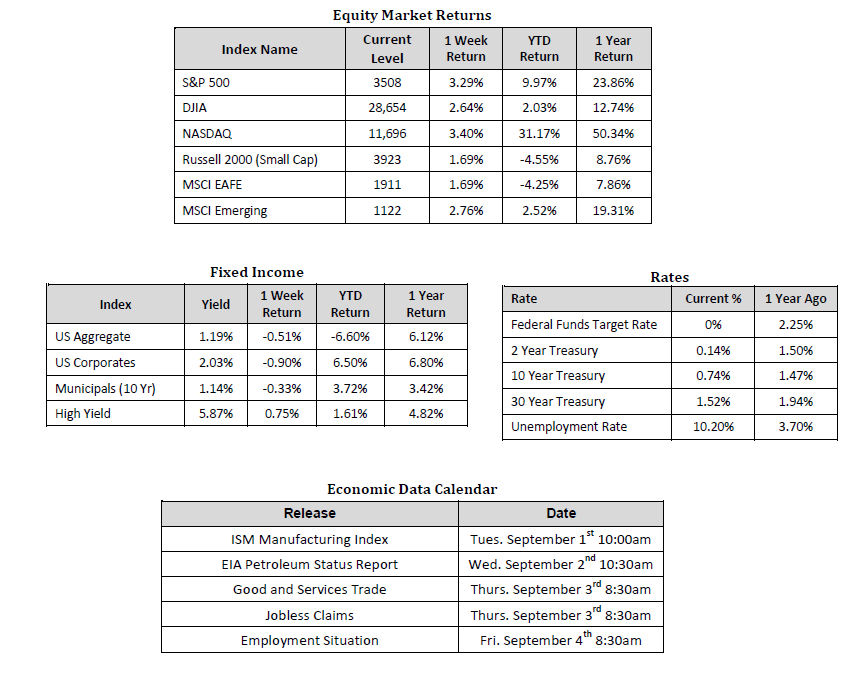

Global equity markets pushed higher on the week, led by the S&P 500 which rose to a new all-time high. In the U.S., the S&P 500 Index rose to a level of 3,508, representing a gain of 3.29%, while the Russell Midcap Index pushed 2.39% higher last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 1.69% over the week. Moreover, developed and emerging international markets returned 1.69% and 2.76%, respectively. Finally, the 10-year U.S. Treasury rallied to 0.74%, 10 basis points higher than the prior week.

Prior to the spread of COVID-19, many may have understandably been unaware of, or unfamiliar with, the iShares iBoxx U.S. Investment Grade Corporate Bond ETF (Ticker: LQD), but that unfamiliarity may have dissipated following the Federal Reserve’s decision to provide liquidity to the U.S. corporate bond market by making secondary market purchases of U.S. corporate bond ETFs through a newly established entity called the Secondary Market Corporate Credit Facility (SMCCF). For those still unfamiliar, the iShares U.S. corporate bond ETF (LQD) is a passively managed index fund that attempts to track the U.S. investment-grade fixed income market’s performance as closely as possible. LQD is also one of 16 U.S. fixed-income ETFs that the Federal Reserve has purchased to influence capital markets positively.

In a perfect world, the performance of LQD will track the performance of the Barclays U.S. Investment-Grade Corporate Bond index identically, producing a return that is no greater, nor less, than the underlying index. Thankfully for those of us who rely on LQD for exposure to this ever-important segment of the global bond market, the ETF has a long history of mirroring the U.S. corporate bond market very closely. Nonetheless, some may be surprised to learn that the composition of the underlying index tracked by LQD has undergone gradual change over the last decade, and that change has accelerated at a rapid pace over the previous six months. The change that we’re referring to is the duration of the U.S. investment-grade bond market. Investopedia.com defines duration as a measure of the sensitivity of the price of a bond to a change in interest rates. Analyzing the current duration, or interest rate sensitivity, of the Bloomberg Barclays U.S. Corporate Bond Index, an index very similar to the underlying index that is tracked by LQD, confirms that duration has meaningfully increased over the past year. In fact, the chart below shows that the Option Adjusted Duration (OAD) of the Bloomberg Barclays U.S. Corporate Bond Index has gradually increased over the past decade and has rapidly accelerated over the last year. So what’s responsible for this increase in interest rate sensitivity, and should impacted investors be concerned?

Source: Bloomberg

As many may remember, part of the Federal Reserve’s response to the economic downfall caused by the COVID-19 pandemic, and associated shutdowns, was to follow the playbook established in the aftermath of the Great Financial Crisis of 2008 and lower certain benchmark interest rates to a range of 0.00%-0.25%. When the Federal Reserve takes such action and makes clear that they have no intention to increase benchmark interest rates for the foreseeable future, it can have a knock-on effect that works to lower intermediate and longer-dated interest rates as well. The natural reaction of U.S. Corporations is to take advantage of what are historically rock bottom lending rates by increasing longer-dated debt issuances. The result is a U.S. corporate bond market with a longer average maturity than what investors have become accustomed to over the last 20 years.

Longer average index maturity coincides with higher duration, which equates to more interest rate sensitivity. However, in our view, those investing in the U.S. investment-grade corporate bond market should not necessarily be overly concerned with elevated interest rate sensitivity (I.e., duration) at this time. If the Federal Reserve is to be taken at their word, we can assume that short term interest rates, represented by the Federal Funds Target Rate, will remain near 0% for at least the next two years and possibly beyond. Furthermore, Fed Chairman Jerome Powell has spoken repeatedly about the Federal Reserve’s willingness to implement “Curve Controls,” which essentially means that they won’t allow any portion of the treasury yield curve to rise above what would be considered economically simulative levels.

Even though we’re not overly concerned with interest rates spiking higher in the near-term, we, of course, recognize that capital markets can be unpredictable, and one way to help temper unpredictability in an investment portfolio is through the use of diversification. As a result, we encourage investors to stay disciplined and work with experienced financial professionals to help manage their portfolios through various market cycles within an appropriately diversified framework that is consistent with their objectives, time-frame, and tolerance for risk.

We recognize that these are very troubling and uncertain times, and we want you to know that we are always here to help in any way we can. Please stay safe and stay well.

Sources for data in tables: Equity Market and Fixed Income returns are from JP Morgan as of 8/28/20. Rates and Economic Calendar Data from Bloomberg as of 8/28/20. International developed markets measured by the MSCI EAFE Index, emerging markets measured by the MSCI EM Index, U.S. Large Cap defined by the S&P 500. Sector performance is measured using GICS methodology. S&P 500 sector performance represents total return figures sourced from Bloomberg.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index.

Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against loss.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than the original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.