Tariffs and Budget Developments Share the Headlines

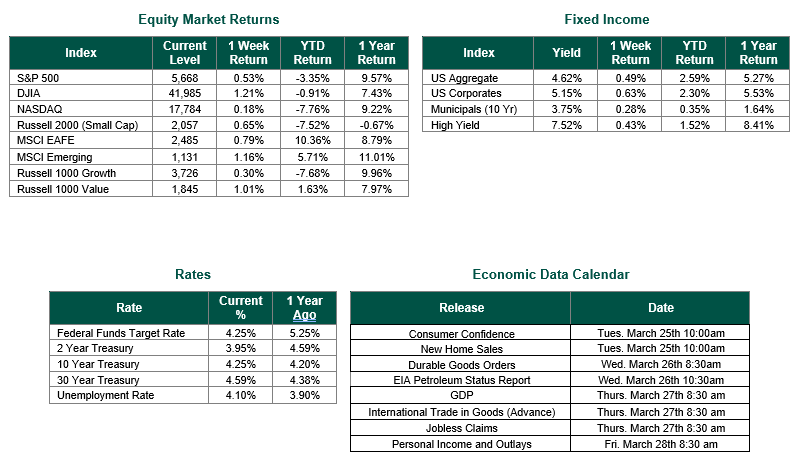

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index closed the week at a level of 5,803, representing a decline of -2.58%, while the Russell Midcap Index moved -2.07% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -3.45% over the week. Developed international equity performance and emerging markets were positive, returning 1.44% and 3.09%, respectively. Finally, the 10-year U.S. Treasury yield remained unchanged, closing the week at 4.47%.

With Memorial Day just past, we like to take a moment to honor the brave men and women who have served our nation with courage and sacrifice. Their dedication has shaped the freedoms we cherish, and their legacy remains a guiding force in our communities.

With a light week for economic data, markets were more focused on Washington DC. Markets reacted to continuing developments in the budgetary process and international trade tariff negotiations. Throughout the remainder of this Update, we will provide insight on all the above topics.

Last week, the U.S. economic landscape was shaped by key data releases that provided insight into labor market conditions, business activity, and housing trends. Jobless claims came in at 230,000, slightly up from the previous week’s 229,000, signaling a modest increase in unemployment filings. Meanwhile, the S&P Global Composite PMI, which combines manufacturing and services sector performance, registered at 53.5, down from 54.3, indicating a slight slowdown in overall business activity. In the housing market, existing home sales rose to 4.13 million, reflecting a 2.7% increase from the prior month, suggesting some resilience despite ongoing affordability challenges. However, new home sales declined to 695,000, marking a 4.0% drop, as higher mortgage rates continued to weigh on buyer demand. These figures collectively painted a picture of an economy experiencing mixed signals, with some sectors showing resilience while others faced headwinds.

The House narrowly passed a sweeping budget bill known as the “One Big Beautiful Bill Act”. The bill includes major tax cuts, increased border security funding, and defense spending, while also imposing stricter work requirements for Medicaid, which could lead to millions losing health coverage. Additionally, it raises the debt ceiling by $4 trillion and eliminates taxes on tips and overtime. The bill now heads to the Senate, where Republicans are expected to push for further modifications before it can be signed into law.

International trade negotiations saw significant developments, particularly regarding U.S. tariff policies. President Trump reached an agreement with China to reduce tariffs by 115%, while both nations retained an additional 10% baseline tariff. This move aimed to ease tensions and open market access for American exports. Additionally, China agreed to suspend retaliatory tariffs and non-tariff countermeasures imposed earlier in April.

Recent developments in U.S.-EU tariff negotiations have taken a dramatic turn. President Trump initially threatened to impose a 50% tariff on all European imports starting June 1, citing stalled trade discussions. However, following a phone call with European Commission President Ursula von der Leyen, Trump agreed to delay the tariff hike until July 9 to allow for further negotiations.

The European Union has responded by fast-tracking trade talks with the U.S., aiming to avoid a full-scale trade war. While discussions have resumed, key sticking points remain, including EU agricultural subsidies and the European Value Added Tax, which the U.S. claims unfairly disadvantage American goods.

As we move forward, the interplay between policy decisions, economic indicators, and global trade negotiations will continue to shape market sentiment and investor confidence. While recent developments in Washington and international trade bring both opportunities and uncertainties, staying informed and adaptable remains key in navigating this evolving landscape. In the coming weeks, we will monitor how these discussions unfold, assess their potential impact, and provide ongoing insights to help make sense of the shifting economic terrain.

Best wishes for the Week ahead.

Equity and Fixed Income Index returns sourced from Bloomberg on 5/23/25. Weekly jobless claims data sourced from the U. S. Department of Labor. PMI data sourced from S&P Global. Existing home sales sourced from the National Association of Realtors. New Home sales sourced from the U.S. Census Bureau. Economic Calendar Data from Econoday as of 5/23/25. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.