Last Week’s Markets in Review: Top Investment Themes for 2022

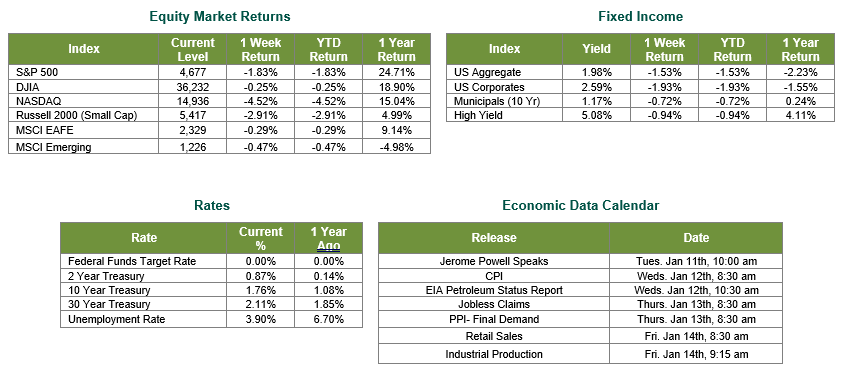

Global markets finished the first week of 2022 in the red. The S&P 500 closed the week at a level of 4,677, representing a loss of 1.83%, while the Russell Midcap Index moved 2.79% lower. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -2.91%. International equity performance also struggled as developed and emerging markets returned -0.29% and -0.47%, respectively. Finally, the 10-year U.S. Treasury yield moved 24 basis points higher over the week, closing at 1.76% on Friday.

As you may recall, our overall macro theme for 2021 was “The Reopening of the Global Economy.” The theme proved true as 2021 was a year marked by a sharp uptick in earnings and economic growth as the economy began its reopening process from the COVID-19 pandemic shutdown. 2021 was also a year that saw significant stock market returns (specifically in the U.S.), excessive valuations, record-setting inflation, supply chain issues, labor supply shortages, a patient Federal Reserve, and two new variants of COVID-19.

We see the theme for 2022 as being “Still Growing but yet Slowing” as it relates to both economic and stock market growth. This theme may ultimately prove to be the case for inflation as well as the new year progresses. In this regard, we would like to share our “Top 10 Investment Themes for 2022” in this week’s update. Details on three of the Top 10 themes are provided below.

1. Investing for a Rising Rate Environment – based on the Federal Reserve’s pivot at the end of 2021, it appears as though they may now be adopting a more hawkish stance to removing the stimulus provided during the COVID-19 pandemic while helping to combat non-transitory areas of inflation. The “Dot Plot” chart that was released after their December 2021 FOMC meeting shows the median forecast of FOMC voting members projecting three rate hikes of 25 Bp each in 2022, another three rate hikes of 25 Bp each in 2023, and two additional rate hikes of 25 Bp each in 2024. While it seems unlikely that there will be three rate hikes in 2022 at this time, and those that do occur will likely occur no earlier than the 2nd quarter, it is fair to conclude that we are entering a rising rate environment. Asset classes that have historically performed well during periods of rising interest rates include, but are not necessarily limited to, equities, high yield bonds, precious metal miners, and convertible bonds.

2. The E-commerce Growth Story Continues – the transition from traditional, in-person retail sales to online sales was well underway before the COVID-19 pandemic due, in large part, to the speed and convenience of shopping online. This transition has only accelerated through the pandemic. Consider that E-commerce sales accounted for just 4.2% of total U.S. retail sales in Q1 2010 and recently accounted for over 13% in Q3 2021, according to Statista. It is also estimated that a record $207 billion will be spent online in the U.S. during the 2021 holiday shopping season. Additionally, it is forecasted that E-commerce will account for nearly 22% of all retail sales globally by the end of 2024. As a result, it has become abundantly clear that E-commerce is not just a fad or a seasonal story but rather represents an ongoing growth narrative with many associated investment opportunities. In our view, these opportunities exist for traditional E-tailers and other companies that derive revenues from their role in the overall E-commerce ecosystem, such as payment providers, Industrial REITs, and air freight & logistics firms.

3. Financials Positioned to Perform as Rates Rise and the Economy Expands – The banking industry maintains a unique and prominent position within the U.S. economy. This critical component of the U.S. economy, notably the smaller-cap regional banks and mortgage and thrift institutions, is also worthy of investment consideration as technology transforms the banking industry, enhancing operational efficiencies and profitability. In addition, changing consumer preferences allow best-in-breed institutions to adapt, grow, and ultimately succeed. These ongoing trends in technology advances and consumer preferences will likely keep industry consolidation at an elevated level throughout 2022, following a year that saw the return of robust M&A activity within the Financial Sector in 2021. Finally, Financials historically have strong performance in a rising rate environment when economies are expanding.

Overall, macro conditions and company fundamentals remain supportive and we see continued appreciation potential for stocks in the new year, albeit to a lesser extent compared to the annual returns over the past three years. As always, we encourage investors to work with experienced financial professionals to help navigate the capital markets and build and manage the asset allocations within their portfolio strategies consistent with their objectives, timeframe, and tolerance for risk. Happy Holidays, and best wishes for the week, and year, ahead!

Sources for data in tables: Equity Market and Fixed Income returns are from JP Morgan as of 1/7/22. Rates and Economic Calendar Data from Bloomberg as of 1/7/22. International developed markets measured by the MSCI EAFE Index, emerging markets measured by the MSCI EM Index, U.S. Large Cap defined by the S&P 500. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.

Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against loss.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than the original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market, and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.