More Stock Market Record Highs as Stagflation Fears Intensify

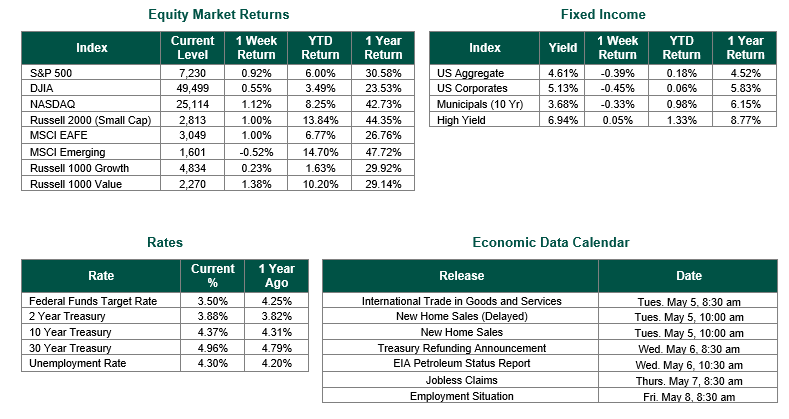

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 7230, representing an increase of 0.92%, while the Russell Midcap Index moved +0.41% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned +1.00% over the week. As developed international equity performance and emerging markets were mixed, returning 1.00% and -0.52%, respectively. Finally, the 10-year U.S. Treasury yield closed the week at 4.37%.

It was a week defined by big earnings beats and an even bigger inflation surprise. Despite turbulence on Tuesday when a report flagging weakness at a major artificial intelligence (AI) company snapped an 18-day winning streak for semiconductor stocks, markets recovered and finished the week broadly positive. Earnings were the dominant driver as the Q1 blended earnings growth for the S&P 500 now stands at 27.1%, the strongest since Q4 2021, with 84% of reporting companies beating estimates, the highest rate in nearly five years, according to FactSet. Technology stocks led the week’s gains, with strong cloud and AI-related results powering the recovery. Several consumer discretionary names also contributed positively, with resilient spending data supporting results across retail and payments. The Nasdaq Composite index crossed 25,000 for the first time in history on Friday, powered by a record-breaking services revenue print from a major technology company. Oil briefly crossed $100 per barrel early in the week before pulling back amid mixed signals from Iran.

The April 28-29 FOMC meeting was widely expected to be routine. It was anything but. The Fed held rates steady at 3.50-3.75%, the third consecutive hold, but the vote split 8-4, the most dissents at any FOMC meeting since October 1992. Three of the four dissenters were not pushing to cut rates; rather, they opposed the Fed’s continued “easing bias” language in the statement, signaling they see no path to lower rates in the current environment. A fourth dissenter voted for an immediate 25 basis-point cut. Current Fed Chair Powell held his final press conference as Fed Chair last Wednesday afternoon, a moment he closed with a reflection on Fed independence, saying the central bank must make decisions “based on analysis rather than political outcomes.” Powell confirmed he will remain on the Board of Governors indefinitely, describing ongoing legal proceedings as leaving him “no choice.” Kevin Warsh, Trump’s nominee to succeed Powell, advanced out of the Senate Banking Committee the same morning, with his confirmation now appearing likely before the next FOMC meeting scheduled for June 16-17.

Thursday’s simultaneous release of Q1 Gross Domestic Product (GDP) and March Personal Consumption Expenditures (PCE) data was the week’s most consequential economic moment. On growth: Q1 GDP came in at 2.0% annualized, a meaningful rebound from Q4 2025’s 0.5% pace, but slightly below the 2.3% consensus estimate. The acceleration was driven by a recovery in government spending, a bounce from the prior quarter’s shutdown-related drag, as well as strength in investment and exports. Consumer spending growth moderated to 1.6%, though final sales to private domestic purchasers, a cleaner read on underlying demand, grew a healthy 2.5%. On inflation: the picture was more concerning, though not entirely surprising. The PCE price index surged to 3.5% year-over-year in March, up sharply from 2.8% in February, with energy costs tied to the Iran conflict driving much of the move. More concerning, core PCE, which excludes food and energy and is the Fed’s preferred inflation gauge, accelerated to 3.2% year-over-year, well above the Fed’s 2% target. The combination of moderating growth and re-accelerating inflation intensified lingering stagflation risks that investors have feared all year.

The April nonfarm payrolls report, due later this week, will be the next major test of the labor market’s durability. Earnings season continues at a heavy pace, with more major technology, consumer, and industrial names reporting through the week. The June 16-17 FOMC meeting is rapidly becoming the next focal point for monetary policy, and with inflation now running well above target and a new Fed Chair likely in place, the debate will intensify over whether the next move is a hold, a hike, or a cut.

Best wishes to all for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 5/1/26. GDP and PCE data sourced from the Bureau of Labor Statistics on 4/30/26. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio, but it does not ensure a profit or guarantee against a loss.