Oil and Jobs Rattle Markets

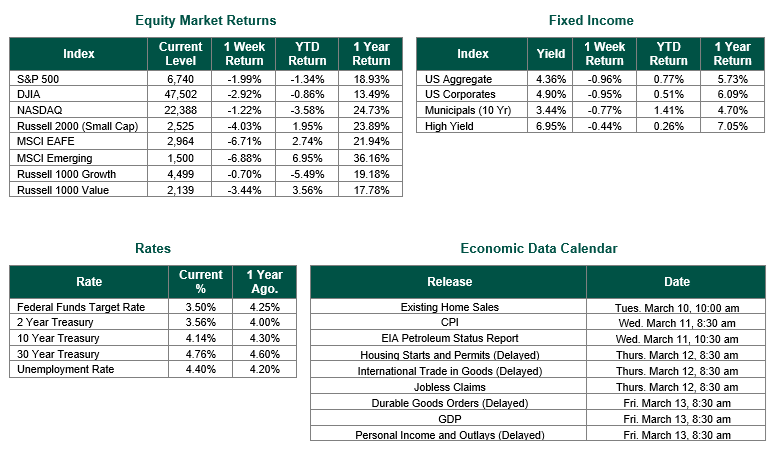

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index closed the week at a level of 6740, representing a decrease of 1.99%, while the Russell Midcap Index moved -3.66% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -4.03% over the week. As developed international equity performance and emerging markets were negative, returning -6.71% and -6.88%, respectively. Finally, the 10-year U.S. Treasury yield closed the week at 4.13%.

It was another painful week for many investors on Wall Street, with the S&P 500 posting its worst weekly decline in nearly 5 months. The index is now down 1.5% on the year and sits 3.4% off its January all-time high. Of course, it is still noteworthy to recognize that the S&P 500 is up 18.93% over the last 1-year. Two forces converged to drive the selling last week: 1) a continued geopolitical shock from the U.S.-Iran conflict and 2) a disappointing jobs report. Volatility spiked sharply, with the VIX surging to nearly 30 as investors sought safety. Energy was the lone sector to post gains on the week, as surging oil prices lifted the sector while nearly everything else declined.

The dominant story of the week was the escalating U.S.-Iran conflict, which rattled global markets and sent oil prices surging. Brent crude climbed from roughly $70 to over $92 a barrel by Friday (with oil prices rising above $100 a barrel over the weekend for the 1st time since 2022). The threat of a prolonged disruption to shipping through the Strait of Hormuz, a chokepoint for approximately one-fifth of global oil and natural gas supply, fueled the move. President Trump sought to calm markets midweek by pledging that the U.S. Navy would escort tankers through the Strait if necessary, helping to pare what had been a more severe intraday selloff on Tuesday. Still, the conflict remained unresolved heading into the weekend, keeping markets on edge.

Friday’s February jobs report piled on to the heap of concerns. It was announced that the U.S. economy shed 92,000 jobs last month — well below the consensus estimate of a 50,000 gain and a sharp reversal from January’s 126,000 gain. The unemployment rate ticked up to 4.4%, which, interestingly enough, is where the Federal Reserve forecasted it would be at the end of 2026 back in December 2025. Making matters worse, prior months’ job gains were revised lower: December’s originally reported gain of 48,000 was revised to a loss of 17,000, meaning payrolls have now contracted in two of the last three months. On net, the U.S. economy has lost jobs since April 2025, painting a different picture of the labor market than was in place just a few weeks ago.

The combination of rising oil prices and a weakening labor market puts the Federal Reserve in a difficult position heading into its March 17-18 meeting. Markets are pricing in a near certainty over 95% probability that the Fed holds rates steady at the upcoming meeting, according to the CME group. Analysts now expect the first cut to take place no earlier than July. A new challenge that has emerged for the Federal Open Market Committee (FOMC) is that if energy prices stay elevated, inflation could re-accelerate just as the labor market softens – a scenario that limits the Fed’s ability to respond to either problem effectively.

With oil hovering near/above $100 and the Iran conflict still unfolding, geopolitics will remain front and center this week and likely for the balance of this month. The Fed’s March 17-18 meeting is the next major calendar event, and Chair Powell’s post-meeting remarks will be closely scrutinized for any shift in tone. Investors will also be watching for any resolution or escalation of the conflict in the Middle East, as the duration of the conflict is now the single biggest variable for both energy prices and the rate outlook.

Equity and Fixed Income Index returns sourced from Bloomberg on 3/6/26. Jobs data was sourced from the Bureau of Labor Statistics. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.