Perspective and Lessons from the Latest Selloff in Stocks

Market Overview

Happening Now

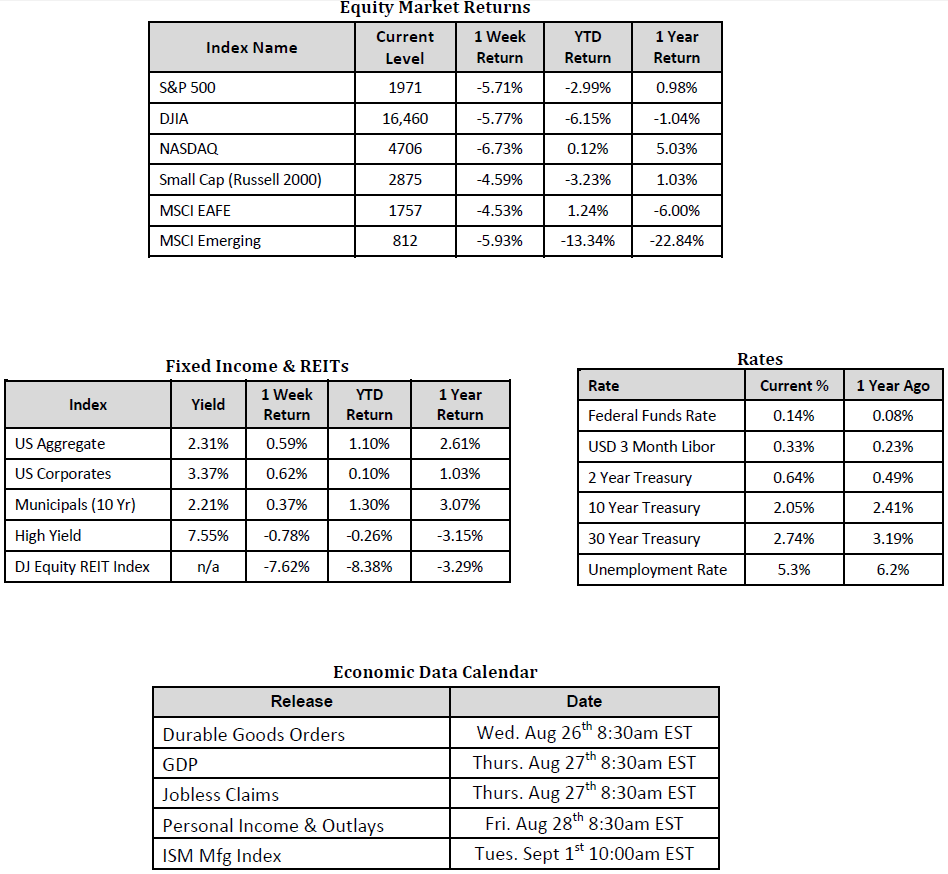

Global equity markets fell at a rapid pace last week with negative sentiment spilling over into Monday’s trading. This is causing many market participants and Wall Street strategists to reevaluate the sustainability of the now 6 ½ year old bull market run. The Dow Jones Industrial Average has now fallen over 13% from its peak this year, the MSCI EAFE (a gauge of developed international markets) has dropped over 15%, and the MSCI Emerging Markets Index is down almost 29%. All three gauges are now in “correction” territory- defined a decline in prices of 10% or more from a prior peak.

What appears to be missing, however, is the smoking gun or reason for the precipitous decline we’ve witnessed, at least as it relates to the U.S. Stock Market. Of course falling energy prices, concern of a hard landing in China, geopolitical risks, the uncertainty in the future of the Euro and questions about the timing of the Fed Funds rate hike, have all been suggested but none are projecting vastly different characteristics or trends relative to a month ago. We, at SmartTrust, cannot conclude from the market’s movements alone and without confirmation from other economic data that the past week’s decline in stock prices will serve as a catalyst propelling the U.S. into a recession or, for that matter, into a prolonged bear market. Even considering the sharp fall in China’s mainland stock market, there appears to be few economists that suggest China is in store for a hard landing. To this end, the macro-economic research firm Capital Economics wrote in a piece Tuesday morning, “… the bursting of the bubble in China’s stock market is unlikely to have much of an adverse effect on her own economy, let alone that of the US.” The rationality for the selloff in stocks (which may not be over) will perhaps be better understood once the dust settles and stability returns but for now it is imperative to be disciplined and not make any rash decisions.

A reasonable case can be made that the market is now more fairly valued. JP Morgan Strategists pointed out yesterday on a conference call that based on Monday’s close, the S&P 500 now has a Forward Price-to-Earnings and Cyclically Adjusted Price-to-Earnings (CAPE or Shiller’s P/E) ratio below the 25 year average as well as a dividend yield of 2.4%, above the 25 year average. This suggests, from a historical prospective, that stocks are oversold at these levels and may provide future upside, simply through multiple expansion.

Individual investors have had the benefit of a 6 ½ year bull market where the S&P 500 index has experienced a cumulative return of over 290%. Over that same period of time volatility fell to historical lows and many individuals became accustomed to the new low risk, high return market environment. The past week is undoubtedly testing everyone’s ability to tolerate market volatility and those that find themselves uncomfortable should be reviewing and more importantly, quantifying the amount of risk they are taking and their exposure to the stock market.

Sources: Equity Market, Fixed Income and REIT returns from JP Morgan as of 8/21/15. Rates and Economic Calendar Data from Bloomberg as of 8/24/15.

Important Information and Disclaimers

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable.

Investing in foreign securities presents certain risks not associated with domestic investments, such as currency fluctuation, political and economic instability, and different accounting standards. This may result in greater share price volatility. These risks are heightened in emerging markets.

There are special risks associated with an investment in real estate, including credit risk, interest rate fluctuations and the impact of varied economic conditions. Distributions from REIT investments are taxed at the owner’s tax bracket.

The prices of small company and mid cap stocks are generally more volatile than large company stocks. They often involve higher risks because smaller companies may lack the management expertise, financial resources, product diversification and competitive strengths to endure adverse economic conditions.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market, and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITSs that primarily own and operate income-producing real estate