Q2 Earnings Season Set to Begin

Market Overview

Happening Now

Lost in the ongoing turmoil over in Greece is the imminent start of the 2015 Q2 earnings season. Alcoa is set to report Wednesday, July 8, 2015 and unofficially kick off the two month time period over which the majority of the U.S.’s publicly traded companies will file their financial statements and hold conference calls with analysts. Prior to the financial crisis, stock returns were primarily driven by fundamentals, most notably earnings and earnings expectations, which are reported quarterly. However, it appears that since 2009 investor focus has been centered on geopolitical, and most recently Federal Reserve, activities with investors’ views on these areas expressed through risk-on/risk-off trading behavior. It should also be noted that given the expansion of profit margins over the past 6 years, which some strategists consider unsustainable, less focus has been given to earnings since, to some, they do not represent an accurate picture of a company’s financial health but rather short term cost cutting to boost the bottom line in certain cases. Perhaps with a resolution (of any kind) in Europe, and after the commencement of rate hikes by the Federal Reserve, enough uncertainties will be removed from the market and we will see a return of fundamentally driven analysis.

Despite the back seat earnings reports have taken as it relates to companies’ stock prices, other metrics such as revenue, or sales, can offer solid insights into a company’s health and future prospects. According to Factset, year-over-year (“y-o-y”) revenue declines for Q2 2015 are expected to be -4.5% which would mark the largest y-o-y fall in revenue since Q3 2009. Interestingly, Factset goes on to point out that seven of the ten sectors that make up the S&P 500 index are expected to show growth in revenue and if the energy sector is removed (which is expected to post a decline of -40.5%), sales growth for companies within the S&P 500 index would be a positive 1.7%.

This highlights the importance of diving deep into fundamentals when selecting equities or evaluating the stock market overall.

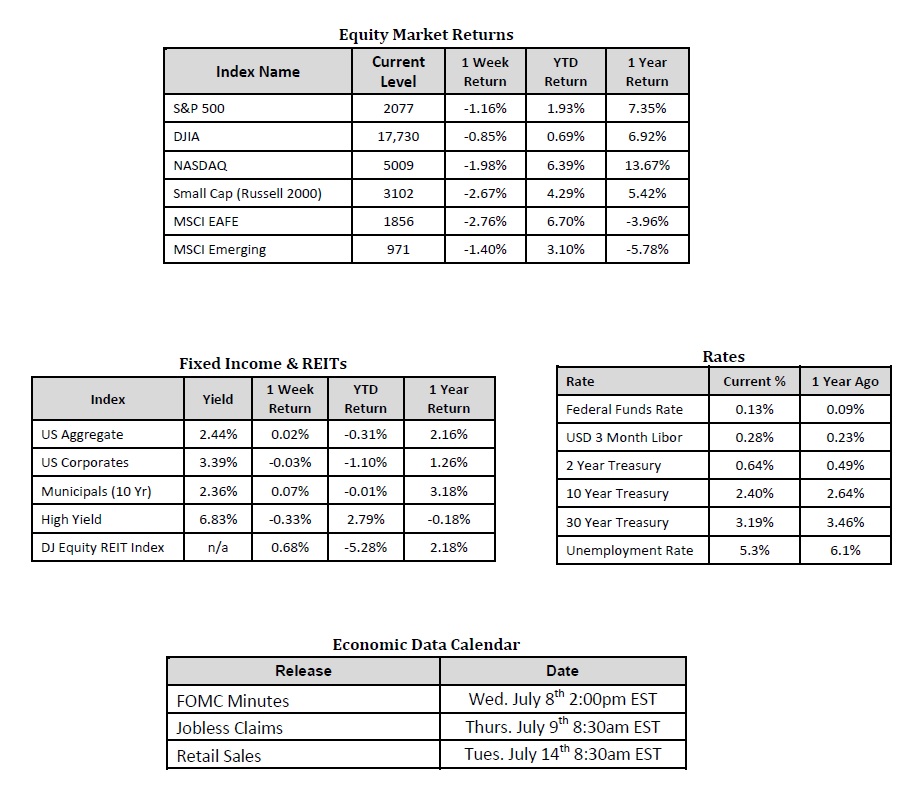

Sources: Equity Market, Fixed Income and REIT returns from JP Morgan as of 7/02/15. Rates and Economic Calendar Data from Bloomberg as of 7/06/15.

Factset: http://www.factset.com/websitefiles/PDFs/earningsinsight/earningsinsight_7.2.15

Important Information and Disclaimers

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable.

Investing in foreign securities presents certain risks not associated with domestic investments, such as currency fluctuation, political and economic instability, and different accounting standards. This may result in greater share price volatility. These risks are heightened in emerging markets.

There are special risks associated with an investment in real estate, including credit risk, interest rate fluctuations and the impact of varied economic conditions. Distributions from REIT investments are taxed at the owner’s tax bracket.

The prices of small company and mid cap stocks are generally more volatile than large company stocks. They often involve higher risks because smaller companies may lack the management expertise, financial resources, product diversification and competitive strengths to endure adverse economic conditions.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market, and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITSs that primarily own and operate income-producing real estate