The Market Rebounds Ahead of Surprising Jobs Data

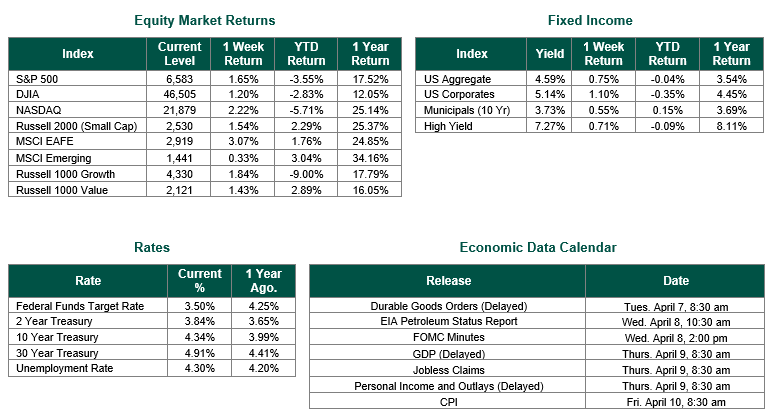

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 6583, representing an increase of 1.65%, while the Russell Midcap Index moved +3.73% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned +1.54% over the week. As developed international equity performance and emerging markets were positive, returning 3.07% and 0.33%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 4.34%.

After five consecutive weeks of losses and the longest losing streak since 2022, markets finally caught a bid. The S&P 500 rose 3.4% on the week, the Dow added nearly 3%, and the Nasdaq surged 4.4%, marking the first weekly gain for all three major indexes since the Iran conflict began. The rally was broad-based, with technology leading the recovery after weeks of disproportionate selling. It was a holiday-shortened week, with markets closed Friday in observance of Good Friday, yet the March jobs report was released Friday morning, but markets won’t be able to fully react until Monday.

The Iran conflict remained the central driver of sentiment throughout the week, though the tone shifted modestly toward cautious optimism. Reports emerged that direct talks between the U.S. and Iran are ongoing through intermediaries, and Iran reportedly released more than 20 oil tankers and submitted a multi-point diplomatic proposal. President Trump set an April 6 diplomatic deadline and acknowledged that “great progress has been made,” though he simultaneously threatened to target Iran’s energy infrastructure if a deal is not reached. Markets responded to the diplomatic signals rather than the rhetoric, helping lift equities off deeply oversold levels. Oil prices remained elevated near $100 per barrel but pulled back from their worst levels, providing some relief to inflation expectations.

The March jobs report, released Friday by the Bureau of Labor Statistics, delivered a meaningful upside surprise. The economy added 178,000 jobs in March — the strongest reading since late 2024 — well above the consensus estimate of approximately 59,000. The unemployment rate edged down to 4.3%. Healthcare led the gains with 76,000 jobs added, largely reflecting workers returning from the Kaiser Permanente strike that had distorted February’s numbers. Construction added 26,000, and transportation and warehousing contributed 21,000. On the downside, federal government employment fell another 18,000, bringing total federal job losses to 355,000, or 11.8%, since the peak in October 2024. Wage growth also moderated, with average hourly earnings rising just 0.2% for the month and 3.5% year-over-year, the slowest annual pace since May 2021.

While the week’s equity gains were welcome, important caveats remain. The S&P 500 still sits roughly 9% below its January all-time high, and the broader labor market picture, despite March’s strong headline, remains fragile. Net job creation has been minimal for over a year, averaging just 68,000 per month in Q1. Oil prices near $100 per barrel continue to act as an inflation tax on consumers and a headache for the Federal Reserve, which is widely expected to hold rates unchanged through the rest of the year. The April 6 diplomatic deadline with Iran is the single most consequential near-term variable: a credible path to de-escalation could meaningfully shift the market outlook, while a breakdown in talks would likely reverse much of this week’s gains.

All eyes turn to the April 6 diplomatic deadline and how markets digest Friday’s jobs report when they reopen Monday. Beyond that, the April 28-29 FOMC meeting looms as the next major policy event, though with inflation still elevated and the Fed firmly on hold, the meeting is unlikely to produce a surprise. With the S&P 500 still down meaningfully on the year, the question heading into the new week is whether this is the start of a sustainable recovery or simply an oversold bounce that fades as the geopolitical and economic headwinds reassert themselves.

Equity and Fixed Income Index returns sourced from Bloomberg on 4/2/26. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.