Inflation, China, the Fed, and Resilient Consumers

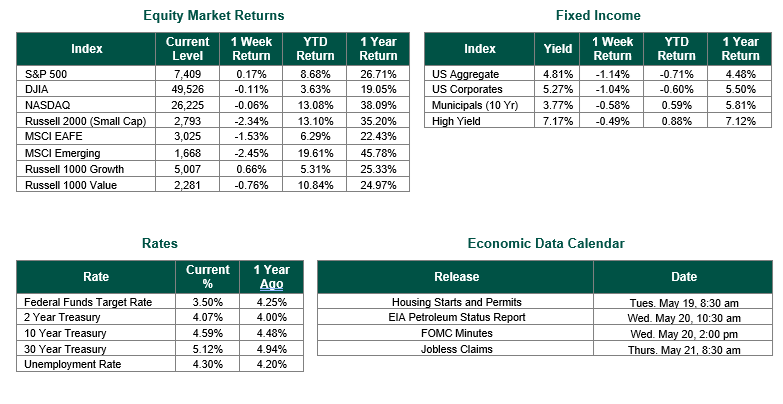

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 7409, representing an increase of 0.17%, while the Russell Midcap Index moved -1.82% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -2.34% over the week. As developed international equity performance and emerging markets were lower, returning -1.53% and -2.45%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.59%.

Last week’s economic data showed that inflation reaccelerated, producer prices remained elevated, consumer demand remained resilient, and labor-market stress remained limited. At the same time, President Trump’s trip to China generated a mix of upbeat trade rhetoric and unresolved strategic issues.

The April Consumer Price Index (CPI) report showed consumer prices rose 0.6% month over month and 3.8% year over year, while core CPI (which excludes the more volatile food and energy prices) rose 0.4% month over month and 2.8% year over year. That combination suggested inflation pressure was broadening rather than being driven by a narrow category such as energy. The PPI report was even firmer, with final-demand producer prices up 1.4% in April and 6.0% year over year, the strongest annual increase since late 2022. Together, CPI and PPI reinforced the view that inflation is accelerating just as markets had hoped for further moderation. Of course, should the Strait of Hormuz reopen to levels seen before the commencement of Operation Epic Fury, oil and gas prices should recede, and inflationary pressures should weaken.

Retail sales for April rose 0.5% month over month to $757.1 billion, matching expectations and marking a third consecutive monthly gain. That strength showed consumers were still spending despite higher prices, although some of the improvement reflected inflation rather than a meaningful acceleration in real purchasing power.

Weekly initial jobless claims rose to 211,000 in the week ending May 9, up 12,000 from the prior week, but remained historically low. That reading was consistent with a labor market that is cooling only gradually rather than deteriorating sharply. As a result, the labor data did little to raise recession fears, even as inflation remained uncomfortably high.

Trump’s China visit produced headlines focused on trade and market access, but the concrete economic impact was less clear. The talks reportedly covered tariffs, rare-earth minerals, Boeing jet orders, Taiwan, and Iranian oil, with Trump touting “fantastic trade deals” and China indicating potential purchases of up to 200 Boeing jets. The delegation also featured major U.S. executives with Chinese officials signaling greater openness to American business. However, many of the outcomes from these talks appeared tentative and more symbolic than structural.

To summarize all of the key data drivers last week, inflation came in hotter, producer prices accelerated, retail spending held up, and jobless claims remained contained, all of which tend to keep upward pressure on yields and reduce the odds of near-term rate cuts (and even make some analysts suggest that rate hikes may be on the horizon). The China trip added a modestly constructive trade sentiment, but it did not materially improve the broader economic backdrop. Kevin Warsh’s Senate confirmation as the new Federal Reserve chairman also added an important policy backdrop, as the transition raises questions about the central bank’s future tone and communication style.

Our thoughts remain focused on the brave men and women of the U.S. Military and our Allies during this conflict in the Middle East.

Equity and Fixed Income Index returns sourced from Bloomberg on 5/15/26. CPI and PPI data are sourced from the U.S. Bureau of Labor Statistics. Retail sales data is sourced from the U.S. Census Bureau. Weekly Jobless Claims are sourced from the U.S. Department of Labor. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio, but does not ensure a profit or guarantee against a loss.