Markets Hit 8 Week Winning Streak Amid Rising Yields and Fed Transition

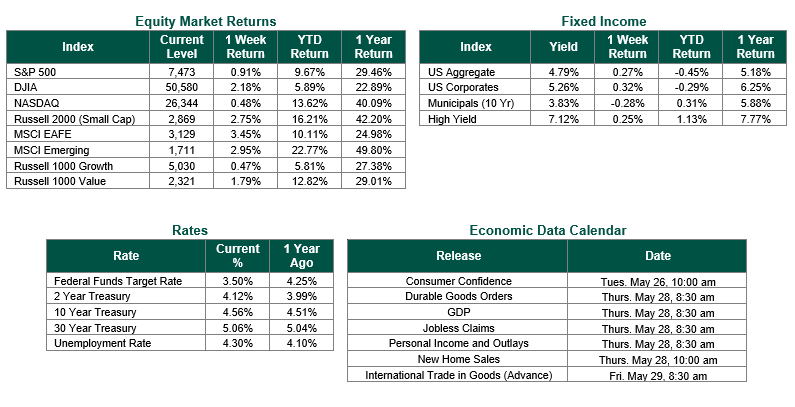

Global equity markets finished positive for the week. In the U.S., the S&P 500 Index closed the week at a level of 7473, representing an increase of 0.91%, while the Russell Midcap Index moved +2.14% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned +2.75% over the week. As developed international equity performance and emerging markets were higher, returning +3.45% and +2.95%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 4.56%.

Last week was a week defined by surging Treasury yields, a leadership transition at the Federal Reserve, and a hotter-than-expected inflation backdrop that further reduced the odds of any rate cuts in 2026. The seven-week winning streak in U.S. equities was tested early in the week as the 10-year Treasury yield climbed to multi-decade highs, pressuring valuations and weighing on the broader market but the market ultimately prevailed. Sentiment improved later in the week after reports of progress in U.S.-Iran negotiations pushed oil prices back below $100 per barrel and helped stabilize interest rates. Energy and defensive sectors led the way, while economically sensitive areas such as materials and industrials lagged. Beneath the index level, the rally remained narrow, with mega-cap technology continuing to do most of the heavy lifting as small-caps and the equal-weight S&P 500 posted only modest gains.

The week’s headline corporate event was Nvidia’s earnings report, which delivered roughly $81.6 billion in revenue (up approximately 85% year-over-year), strong profitability, and an $80 billion stock buyback authorization, reinforcing the view that AI infrastructure spending remains a powerful tailwind, even as expectations grow increasingly stretched.

The formal swearing-in of Kevin Warsh as the new Federal Reserve Chairman, taking the helm at one of the most consequential moments for monetary policy in recent memory was also in focus. Warsh has publicly favored lower rates, but he inherits a divided committee where the April FOMC minutes revealed several members had discussed the possibility of rate hikes, given persistent inflation pressure.

The week ahead is holiday-shortened but data-heavy. Tuesday brings May consumer confidence, Wednesday delivers April new home sales, and Thursday features both the second estimate of Q1 GDP and the April Personal Consumption Expenditures (PCE) report, the Fed’s preferred inflation gauge and the most important release of the week. Given how sensitive markets have become to inflation readings, a hotter-than-expected PCE print would likely reignite the bond market selloff and put additional pressure on equity valuations, while a cooler print could provide meaningful relief. Any commentary from Chairman Warsh in his first week in the role will also be closely scrutinized for clues on the future path of policy.

Equity and Fixed Income Index returns sourced from Bloomberg on 5/22/26. NVDIA earnings sourced from FactSet on 5/20/26. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio, but does not ensure a profit or guarantee against a loss.