Last Week’s Markets in Review: Higher Rate Fears and the Failure of SVB

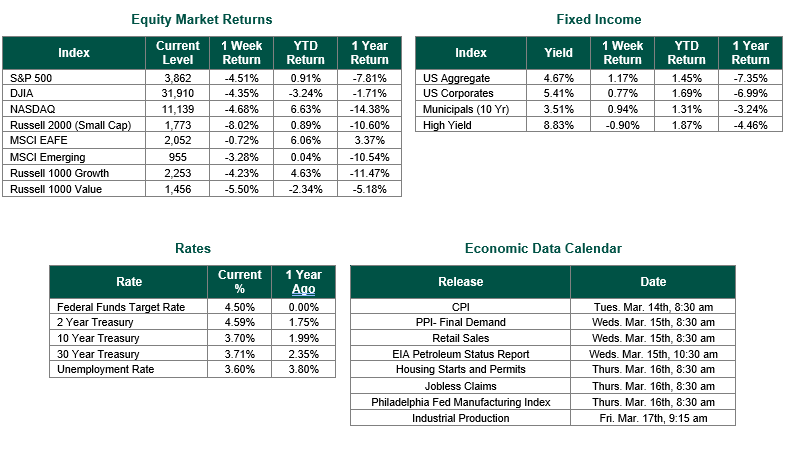

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index closed the week at a level of 3,862, representing a decline of 4.51%, while the Russell Midcap Index moved -6.74% lower last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -8.02% over the week. As developed, international equity performance and emerging markets were lower returning -0.72% and -3.28%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 3.70%.

With recent economic data demonstrating that inflation may have reversed the deceleration it showed in late 2022, market participants were fixated on Fed Chair Powell’s two days of testimony on Capitol Hill. Beginning with the Senate Banking Committee on Tuesday and followed by the house Financial Services Committee the day after.

On Tuesday Powell stated, “The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated.” This statement along with others has forced market participants, which have believed the Fed would falter in its inflation fight, to reassess their own views to match the views of policymakers who have been warning about a higher for longer rate cycle.

By the end of his two days of testimony, Powell had moved both markets and more importantly market opinion about future monetary policy. Markets now believe that the peak of the interest rate cycle, the terminal rate of federal funds is likely to be higher than previous indications from Fed officials and that the switch last month to a smaller quarter-percentage point increase could be short-lived.

The next check on inflation came on Friday with the release of the February Employment Situation Report from the Labor Department. Nonfarm payrolls rose by 311,000, exceeding the consensus estimate of 225,000. The unemployment rate rose to 3.6%, above the expectation for 3.4%. The labor force participation rate rose to 62.5%, its highest level since March 2020. Average hourly earnings, a key statistic in gauging inflation, climbed 4.6% annually, below the estimate for 4.8%. The monthly increase of 0.2% also was below the 0.4% estimate.

In addition to all these topics, the greatest amount of market chaos was centered around the failure of Silicon Valley Bank. In a rapidly developing chain of events, Silicon Valley Bank was closed on Friday by the Federal Deposit Insurance Corporation (FDIC). The details of this failure are still unclear, but it appears that fear and panic within the bank’s deposit base caused a massive wave of deposit withdrawals within a 48-hour window. Reports abound that between Wednesday and Thursday, $48 billion of deposits were withdrawn from the Bank.

Over the weekend, Regulators have approved plans to backstop both depositors and financial institutions associated with Silicon Valley Bank. The Treasury Department designated Silicon Valley Bank and Signature Bank as systemic risks, giving it authority to unwind both institutions in a way it said “fully protects all depositors.” Regulators view this protection as a critical step in stemming a feared systemic panic brought on by the collapse of the 16th largest bank in the U.S. The new Bank Term Funding Program from the Federal Reserve will be very helpful to any bank that needs to enhance liquidity during these uncertain times.

Investors should consider all the information discussed within this market update and many other factors when managing their investment portfolios. However, with so much data and so little time to digest, we encourage investors to work with experienced financial professionals to help process all this information to build and manage the asset allocations within their portfolios consistent with their objectives, timeframe, and tolerance for risk.

Best wishes for the week ahead!

The February Employment Situation Report is sourced from the Department of Labor. Equity Market, Fixed Income returns, and rates are from Bloomberg as of 3/10/23. Economic Calendar Data from Econoday as of 3/10/23. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.