Last Week’s Markets in Review: Politics & S&P 500 Sector Performance

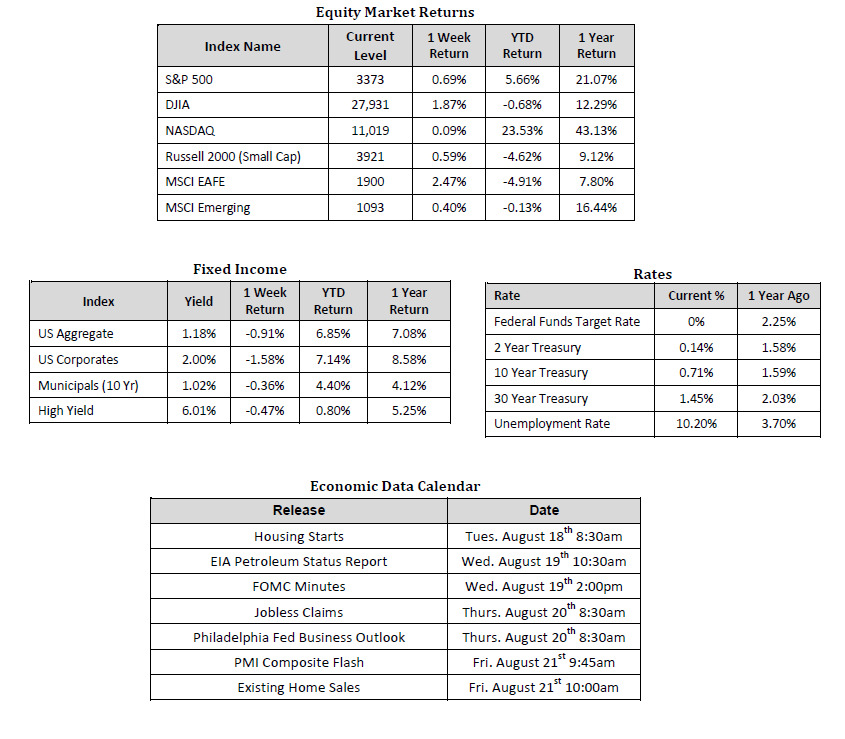

Global equity markets pushed higher on the week, although the S&P 500 index stopped just short of its all-time high which was reached earlier in the year in February. In the U.S., the S&P 500 Index rose to a level of 3,373, representing a gain of 0.69%, while the Russell Midcap Index pushed 0.66% higher last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 0.59% over the week. Moreover, developed and emerging international markets returned 2.47% and 0.40%, respectively. Finally, the most pronounced moves of the week may have come from the 10-year U.S. Treasury which finished the week at 0.71%, 14 basis points higher than the prior week.

On the economic data front, the divergence between consensus expectations and reported results continued, with PPI (Producer Price Index) registering nearly twice as high as anticipated. As a reminder, PPI is provided by the Bureau of Labor Statistics (BLS) and measures the average change, over time, in the prices received by domestic producers of goods and services. By measuring the increase in input costs incurred by producers of goods and services, we are often able to glean the degree to which costs are likely to increase for the end consumer. Turing to CPI (Consumer Price Index) data, which was released later in the week and measures the change in the average price level of a fixed basket of goods and services purchased by consumers, we saw that PPI is, in fact, a good indicator of likely CPI as reported CPI was also twice as high as consensus estimates called for.

Both PPI and CPI were expected to clock in at 0.3% but instead increased by 0.6% from the prior month. Each of these figures came in well above expectations, which is a sign that there might be more inflationary pressure than previously believed. However, contrasting the 0.6% month over month increase in consumer prices against the destructive 16%+ inflationary backdrop of the late 1970s and early 1980s should dissuade any real concern. Finally, on the economic data front, weekly jobless claims came in at 963,000, marking the first time weekly jobless claims registered below a million since the start of the “coronacrisis”.

In political news, the markets digested the announcement of California Senator Kamala Harris as Joe Biden’s running mate. For many investors, the question still remains as to how much attention investors should pay to electoral outcomes and what action, if any, should be taken in one’s portfolio in the lead up to an election? The notion that political risk shouldn’t inform investment decisions may sound completely absurd. In today’s political arena, common ground between the prevailing political parties has been harder to find, which only reinforces the view that elections are life-or-death events that should guide one’s investment strategy. However, at Hennion & Walsh, we’ve written about, and have always contended, that presidential elections, or any election for that matter, should not dictate an investor’s long-term investment strategy and resulting portfolio allocation. A detailed explanation as to how we view and account for political risk can be found here.

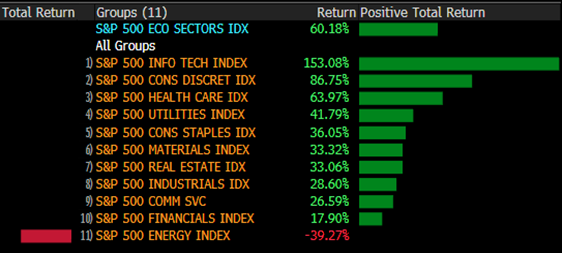

In this week’s market update, we thought it might be interesting to deconstruct and analyze the performance of the S&P 500, and it’s constituent sectors, under President Trump and President Obama’s administrations. Before we dive into the results, please be aware that we’ve compared S&P 500 performance during President Obama’s second term to President Trump’s first term to date, based on the assumption that those consecutive eight years are most likely to provide the best apples to apples comparison. We’re also less concerned with the absolute level of return given the understandable weight that a global pandemic places on total returns. Instead, we are more interested in accessing the composition of sector leaders and laggards.

S&P 500 Sector Performance under President Trump (1/20/17 – 8/12/20)

When analyzing sector by sector performance under each respective administration it would appear that the winners and losers are, for the most part, relatively consistent. Overall performance, and perhaps more interesting sector performance, has essentially been the same under both administrations, despite the perception, and possible reality, that each administration has followed near opposite policy playbooks. So what does this tell us? It likely tells us that certain long-term structural forces are at play, and those forces will most likely continue to usher investor capital toward the technology sector and away from the energy sector as an example, regardless of which political party is in power.

Having a strategy in place that is positioned to take advantage of long-term structural trends in a diversified way aligned with one’s time horizon and risk tolerance is often a solid recipe for success. Conversely, allowing heated political rhetoric to influence one’s investment decisions can tend to lead suboptimal outcomes. As a result, we encourage investors to stay disciplined and work with experienced financial professionals to help manage their portfolios through various market cycles within an appropriately diversified framework that is consistent with their objectives, time-frame, and tolerance for risk.

We recognize that these are very troubling and uncertain times, and we want you to know that we are always here to help in any way we can. Please stay safe and stay well.

Sources for data in tables: Equity Market and Fixed Income returns are from JP Morgan as of 8/14/20. Rates and Economic Calendar Data from Bloomberg as of 8/14/20. International developed markets measured by the MSCI EAFE Index, emerging markets measured by the MSCI EM Index, U.S. Large Cap defined by the S&P 500. Sector performance is measured using GICS methodology. S&P 500 sector performance represents total return figures sourced from Bloomberg.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index.

Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against loss.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than the original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.