Last Week’s Markets in Review: S&P 500 Crosses 5000 Milestone

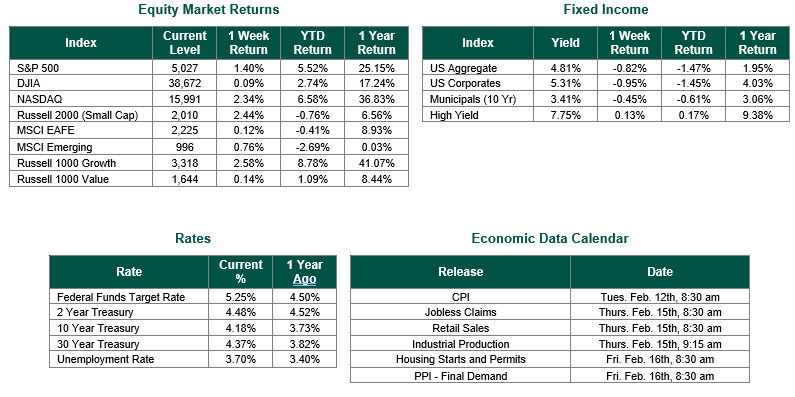

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 5,027, representing an increase of 1.40%, while the Russell Midcap Index moved 1.65% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 2.44% over the week. Developed international equity performance and emerging markets were also positive, returning 0.12% and 0.76%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.18%.

The inception of the S&P 500 index took place over 100 years ago, in 1923, when it tracked 233 companies using a daily 90-day composite. In 1957, Standard and Poor’s expanded from 233 names to include 500 names as its constituted today. At the start, the index traded at a level of 44.06. Last week, the most highly tracked stock index globally surpassed a level of 5,000, a remarkable feat in its 67 year history.

The 5,000 level reached by the index does not have a meaningful statistical relevance, but rather more of a psychological influence on how investors may perceive the current level. Does the record milestone represent overbuying behavior by participants, or is it seen as a catalyst for equity momentum? Let’s take a look at some S&P milestones that may shed some light on this question.

From its starting point of 44.06, it took the index 14,112 calendar days to reach a level of 1,000 on February 2, 1998. From that point in time it took less than half the number of days to reach 2,000 on August 26, 2014 (I.e., just 6,091 days). From 2,000 to 3,000 the index again took less than half the time of the previous milestone point when it took 1,799 days. The 4,000 mark for the S&P again came even quicker than its last 1,000 breakpoint, albeit at a slower relative pace, when it took 997 days between July 12, 2019 and April 1, 2021. Finally, from 4,000 to 5,000 the trend reversed and rather than taking fewer days to enter into another millennium, the index required 1,033 days.

The rapid expansion of the index in the past decade would seem astonishing when considering how long it took to reach the 1,000 and 2,000 milestones. However, the power of compounding returns, ease of access to markets for consumers, wide availability of information, and increasing forms of investment vehicles have allowed equity markets to grow in a vastly different manor than in past decades. Based solely on these technical moves, we should expect the next 20% of growth to the 6,000 level to occur within the next 3 years, a strong momentum driver for equity investors. So, to answer our above question, it may in fact appear that the emotional catalyst of the index milestone could be effective in driving further gains as investors gauge and interpret what it means to reach all-time highs. Of course, past performance is not indicative of future results, and investors should not rely on any one piece of data to make investment decisions.

We hope everyone enjoyed Super Bowl weekend and wish you the best for the week ahead!

Equity Market, Fixed Income returns, and rates are from Bloomberg as of 2/9/24. Economic Calendar Data from Econoday as of 2/9/24. Index milestone dates sourced from Bloomberg on 2/9/24. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.