Last Week’s Markets in Review: Timing the Markets vs. Time in the Markets

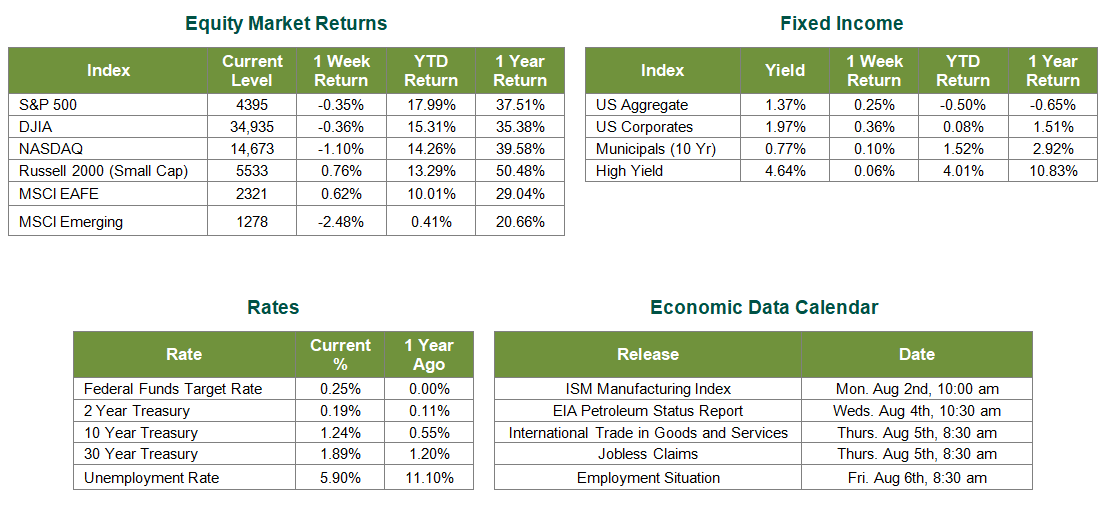

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index reached record highs during midweek sessions but closed the week at a level of 4,395, representing a loss of 0.35%, while the Russell Midcap Index moved 0.41% higher last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 0.76% over the week. International equity performance dragged as developed, and emerging markets returned -0.38% and -2.48%. Finally, the 10-year U.S. Treasury yield ticked lower, closing the week at 1.24%.

As professional asset managers, one of the most common questions we hear is, “is now the time to”…?” with an array of options such as “buy” or “sell” to fill in the blank. With updates around earnings, inflation, interest rates, coronavirus and China, dominating the headlines of late, the concerns about the effects these areas may have on ‘investors’ portfolios has many re-asking the questions mentioned above. Without the help of a crystal ball or a 1982 DeLorean time machine, it very well may be impossible to have the correct answers. Perhaps, when investing, by changing the focus from trying to time the market to maintaining discipline by staying invested in the market, the longer-term effect on portfolios can be significant.

Timing the markets can be highly rewarding or dreadfully painful. Consider the following scenarios, investor #1 timed the market perfectly in 2020 and bought at the bottom on March 23, realizing a 65.19% return on the S&P 500 for the year. Investor #2, on the other hand, hesitated and waited 3 weeks to buy on April 14, ending the year with a 36.33% return, nearly a 29% difference from investor #1. As you can see, there can be a tremendous reward for perfect timing and painful opportunity cost from poor timing, sometimes in just a short period of time. The opportunity to capture these potentially tremendous rewards is something that investors have long been trying to obtain, but attempting to do so can also have serious adverse effects on a portfolio. For this reason, we again would like to draw a focus on time in the market and not timing the market.

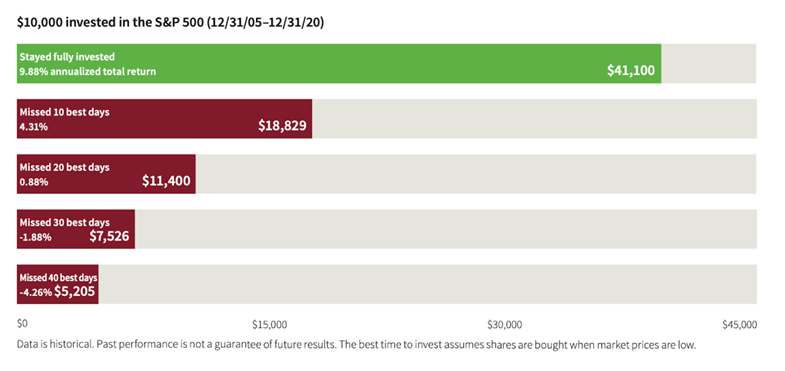

To better illustrate this strategy, let us look at a longer-term situation than our previous example. In the below chart from Putnam investments, we get a clear picture of what investors obtained over the past 15 years by buying and holding the S&P 500 Index. A $10,000 investment would have grown to $41,100. At the same time, by missing out on just 10 of the best trading days over that timeframe, the portfolio would be worth less than half of that in a buy and hold strategy. To underscore this point further, consider that with an average of 253 trading days per year, this significant underperformance can occur by missing just ten days out of 3,795 during this period.

With various forms of uncertainty surrounding markets, it’s understandable why so many investors feel the desire to try and time markets. However, as we have seen, the daunting task of perfectly hitting those moments may very well be futile and not be worth attempting. Instead, we believe that it is essential for investors to speak with financial professionals to ensure that their portfolios are appropriately invested in accordance with their goals, timeframes, and risk tolerances. By maximizing your time in the market, the long-term results may make for a less stressful and less choppy ride.

Sources for data in tables: Consumer Price Index statistics are from the U.S. Department of Labor. Equity Market and Fixed Income returns are from JP Morgan as of 7/30/21. Rates and Economic Calendar Data from Bloomberg as of 7/30/21. International developed markets measured by the MSCI EAFE Index, emerging markets measured by the MSCI EM Index, U.S. Large Cap defined by the S&P 500. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.

Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against loss.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than the original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market, and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.