Last Week’s Markets in Review: Will the Leaders Continue to Lead the Markets Forward?

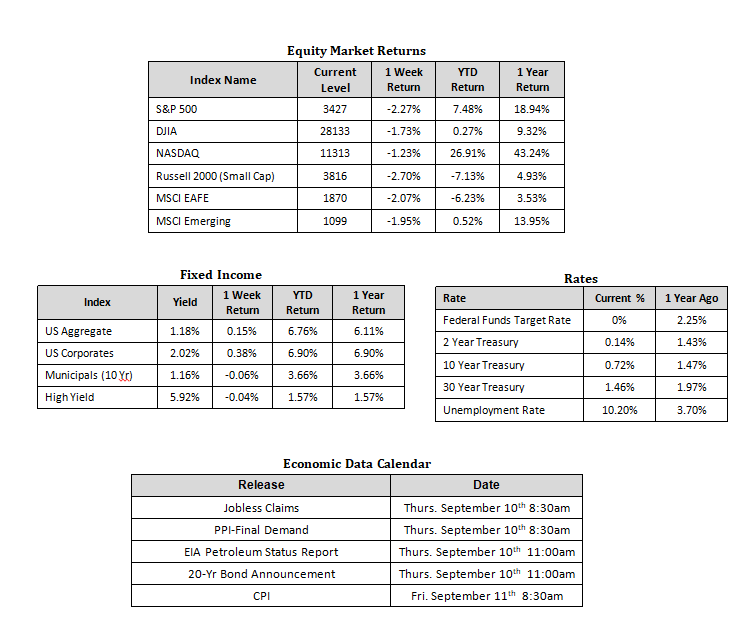

Stocks snapped a five week winning streak as major indexes declined last week. In the U.S., the S&P 500 Index fell to a level of 3,427, representing a loss of 2.27%, while the Russell Midcap Index pushed 1.95% lower last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -2.70% over the week. International equities also lost ground as developed and emerging markets returned -2.07% and -1.95%, respectively. Finally, the yield on the 10-year U.S. Treasury was little changed, finishing the week at 0.72%, down 2 basis points from the week prior.

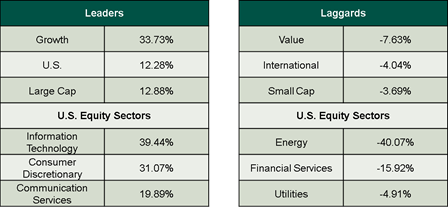

Prior to the sell-off late last week (which is now extending into early this week), equity markets reached new highs and mounted a significant recovery from the lows that were reached in late March. As a result, we thought it appropriate to take a look at which areas of the markets have been driving performance thus far this year, which areas have lagged, and where we see potential opportunities moving forward. We’ve assembled the table below of asset classes, styles, and sectors showing the leaders vs. the laggards.

Source: Bloomberg 12/31/2019 – 9/2/2020

The dispersion of returns within the categories above is incredible. U.S., Large Cap, and Growth stocks have outperformed significantly leading up to and through the COVID-19 selloff and subsequent rebound. Anyone following the financial markets or media is well aware of this, however, the question becomes, where do we go from here? Are valuations stretched, are we “due” for a shift from Growth to Value, or is there greater growth potential in international and small-cap stocks?

Just because the bull market run for stocks has resulted in lofty valuations doesn’t mean that stocks cannot continue to move higher and intermittent pullbacks like we are seeing now shouldn’t be too surprising to investors. Instead, these events suggest that investors may need to become more selective to find pockets of growth opportunities in the months ahead. For example, we don’t necessarily believe a rotational shift from Growth to Value or U.S. to International is imminent based on current valuations alone. We actually tend to favor companies in many of the category leaders listed above and otherwise. But again, this is why we stress selectivity.

At this time some of the areas we favor are innovative and quality U.S. companies, which can be sector agnostic. Examples include companies developing or utilizing revolutionary technologies like cybersecurity and artificial intelligence, along with biotech companies within the Healthcare sector developing innovative technologies to treat and cure chronic diseases. These will undoubtedly involve some small-cap companies. E-commerce should also continue its strong growth trend, which will benefit the online retailers, but also stands to benefit the payment processors, logistics companies, and warehouses that are all involved in, and derive revenues from, the entire e-commerce ecosystem.

Keep in mind, our society continues to evolve at a rapid pace. Introduce a variable like COVID-19 into the equation and the world is forced to change and adapt in order to survive and thrive. We believe that this evolution that has been occurring in areas including technology, e-commerce, and health care, combined with the force of change brought on by the COVID-19 pandemic, will form the basis of the new American economy and is crucial for investors to adjust accordingly.

With so much uncertainty around the future of COVID-19, the economic recovery from the COVID-19 containment measures, and the upcoming November U.S. elections, it is likely that there will be more days of heightened volatility ahead. As a result, we encourage investors to stay disciplined and work with experienced financial professionals to help manage their portfolios through various market cycles within an appropriately diversified framework that is consistent with their objectives, time-frame, and tolerance for risk.

We recognize that these are very troubling and uncertain times and we want you to know that we are always here for you to help in any way that we can. Please stay safe and stay well.

Sources for data in tables: Equity Market and Fixed Income returns are from JP Morgan as of 9/4/20. Rates and Economic Calendar Data from Bloomberg as of 9/4/20. International developed markets measured by the MSCI EAFE Index, emerging markets measured by the MSCI EM Index, U.S. Large Cap defined by the S&P 500. Sector performance is measured using GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index.

Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against loss.

Investing in commodities is not suitable for all investors. Exposure to the commodities markets may subject an investment to greater share price volatility than an investment in traditional equity or debt securities. Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

Products that invest in commodities may employ more complex strategies which may expose investors to additional risks.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than the original cost upon redemption or maturity. Bond Prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment.

Definitions

MSCI- EAFE: The Morgan Stanley Capital International Europe, Australasia and Far East Index, a free float-adjusted market capitalization index that is designed to measure developed-market equity performance, excluding the United States and Canada.

MSCI-Emerging Markets: The Morgan Stanley Capital International Emerging Market Index, is a free float-adjusted market capitalization index that is designed to measure the performance of global emerging markets of about 25 emerging economies.

Russell 3000: The Russell 3000 measures the performance of the 3000 largest US companies based on total market capitalization and represents about 98% of the investible US Equity market.

ML BOFA US Corp Mstr [Merill Lynch US Corporate Master]: The Merrill Lynch Corporate Master Market Index is a statistical composite tracking the performance of the entire US corporate bond market over time.

ML Muni Master [Merill Lynch US Corporate Master]: The Merrill Lynch Municipal Bond Master Index is a broad measure of the municipal fixed income market.

Investors cannot directly purchase any index.

LIBOR, London Interbank Offered Rate, is the rate of interest at which banks offer to lend money to one another in the wholesale money markets in London.

The Dow Jones Industrial Average is an unweighted index of 30 “blue-chip” industrial U.S. stocks.

The S&P Midcap 400 Index is a capitalization-weighted index measuring the performance of the mid-range sector of the U.S. stock market and represents approximately 7% of the total market value of U.S. equities. Companies in the Index fall between S&P 500 Index and the S&P SmallCap 600 Index in size: between $1-4 billion.

DJ Equity REIT Index represents all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as Equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.