Markets Hit Record Highs as Lasting Ceasefire Hopes Take Hold

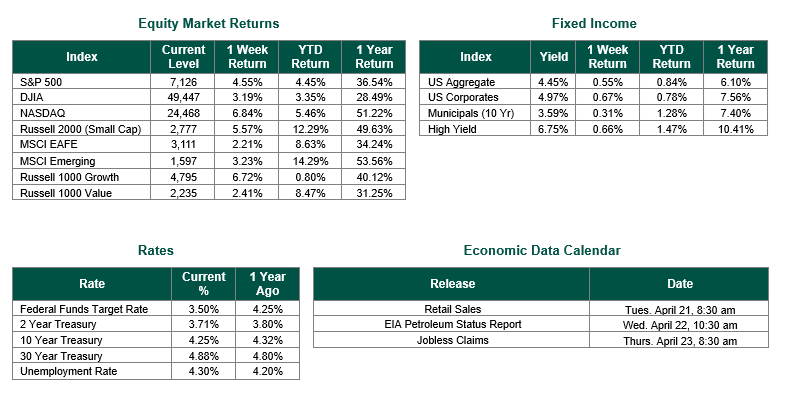

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 7126, representing an increase of 4.55%, while the Russell Midcap Index moved +2.17% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned +5.57% over the week. As developed international equity performance and emerging markets were positive, returning 2.21% and 3.23%, respectively. Finally, the 10-year U.S. Treasury yield closed the week at 4.25%.

It was a historic week on Wall Street. Despite starting last Monday under pressure from a new U.S. naval blockade of Iranian ports and a spike in oil prices above $100 a barrel, markets showed remarkable resilience throughout the week and finished at record highs. For example, the S&P 500 closed Friday at 7,126, a fresh all-time high, fully recovering all its Iran war losses and then some. In addition, the Nasdaq posted its 13th consecutive winning session on Friday, its longest winning streak since 1992, while the Russell 2000 also touched a new record.

Last week began with a jolt. After weekend peace talks in Islamabad collapsed, the U.S. announced a naval blockade targeting Iranian ports, sending oil prices surging above $104 per barrel in early Monday trading. However, markets quickly shrugged off the initial shock as President Trump struck an optimistic tone, saying the U.S. had been “called by the other side” and that Iran was showing a new willingness to make a deal. By midweek, a second round of negotiations was being discussed, and on Thursday, the president announced a 10-day ceasefire between Israel and Lebanon. Friday delivered the week’s biggest market catalyst: Iran declared the Strait of Hormuz “completely open” for commercial traffic. Oil prices fell sharply: West Texas Intermediate (WTI) Crude Oil dropped over 11% on Friday alone, settling below $84 per barrel. Markets rallied significantly on the news, interpreting the reopening of the Strait as the clearest signal yet that the seven-week conflict may be nearing an end.

The first week of Q1 earnings season provided an encouraging early read. Major financial institutions posted strong results, with earnings and revenue beats, and the early tone from corporate management teams was broadly constructive. Information technology remained the standout sector for the week, with software rebounding sharply from the prior week’s AI-disruption fears. The Philadelphia Fed’s Manufacturing Survey, released last Thursday, also beat expectations, showing regional activity expanded at its fastest pace in months – though its prices-paid component hit its highest reading since August 2025, a reminder that cost pressures have not fully dissipated.

Earnings season accelerates this week with major technology, consumer, and industrial companies scheduled to report. The April 28-29 FOMC meeting is also approaching, and with oil prices falling and core inflation contained (for now), the Fed may find itself with slightly more room to maneuver than markets had assumed just weeks ago. The Iran ceasefire remains the key wildcard — it is fragile and unconfirmed by independent shipping data, and any breakdown in the peace process would almost certainly reverse a significant portion of this week’s gains. But for now, markets have delivered a decisive verdict: after the most volatile quarter since 2022, investors appear to be looking forward and becoming optimistic (again) about stocks.

Best wishes to all for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 4/17/26. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.