Micron Earnings Show AI Revolution is Alive and Well (For Now)

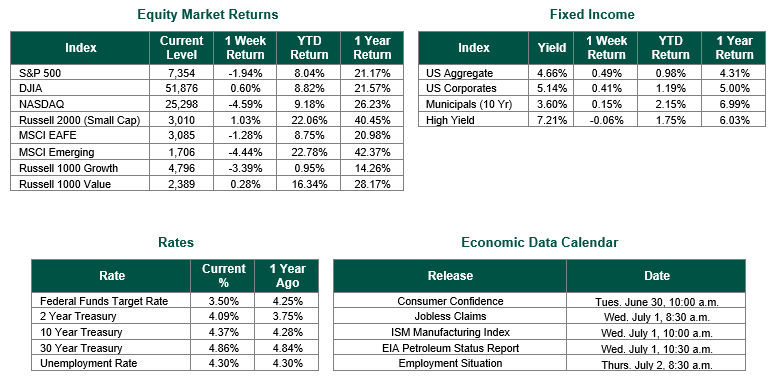

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 7354, representing a decrease of 1.94%, while the Russell Midcap Index moved +0.97% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned +1.03% over the week. As developed international equity performance and emerging markets were negative, returning -1.28% and -4.44%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 4.37%.

Micron Technology Inc. reported record earnings last week, which showed investors that the artificial intelligence (AI) revolution is alive and well. Micron, an industry-leading supplier of memory and storage chips, saw its stock price soar after its third-quarter earnings beat expectations. In particular, Micron reported adjusted earnings of $25.11 per share (topping the $20.78 expected by analysts polled by LSEG) and quadrupled its revenue from the previous year to $41.46 billion. While investors will likely continue to poke at a perceived “AI bubble,” earnings and order backlogs from companies such as Micron and Nvidia suggest to us that the AI infrastructure buildout is still in its early stages.

Aside from Micron, U.S. economic data released last week painted a picture of a resilient yet transitional economy, highlighted by an upward revision to Q1 Gross Domestic Product (GDP) growth to an annualized 2.1%. This final revision, up from the previously reported 1.6%, was primarily driven by a drop in imports, comfortably offsetting a slight cooling in consumer spending. Production and business metrics signaled solid momentum, as the S&P Global Flash Purchasing Managers’ Index (PMI) for June climbed to a five-month high of 52.2, led by a sharp acceleration in manufacturing activity to its highest level since May 2022. However, this expansion was met with some corporate caution as new orders for manufactured durable goods pulled back by 4.5% in May. Firms continued to seemingly tighten their belts, leading to a second consecutive month of softer employment data amid stubborn supply chain friction.

On the consumer side, the financial picture remains relatively stable, but inflationary pressure persists. Data from the U.S. Bureau of Economic Analysis (BEA) showed that both personal income and personal spending surged by 0.7% in May, beating consensus expectations and underscoring that consumer demand remains a sturdy (and necessary) backbone of the broader economy. This aggressive spending came alongside anticipated increases in the Federal Reserve’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) price index, which grew 0.4% for the month, keeping the annual headline inflation rate elevated at 4.1%. Labor markets continued their gradual normalization, with initial weekly jobless claims holding steady at 215,000. It should be pointed out that the most recent GDPNow forecast for the 2nd quarter of 2026 from the Federal Reserve Bank of Atlanta was revised downward to 2.5%.

The latest economic data reinforces the Federal Reserve’s recent pivot toward a more neutral/slightly hawkish “higher-for-longer” monetary policy under newly appointed Chair Kevin Warsh. During its June 2026 FOMC meeting, the committee voted unanimously to maintain the benchmark federal funds rate at 3.50% to 3.75%. However, the economic reality reflected in last week’s indicators strongly justifies the Fed’s complete scrubbing of its previous rate-cutting bias from its official policy statement.

The primary catalyst likely driving the Fed’s next decision at the end of July will be stubborn, sticky inflation, which directly threatens their 2% long-term goal. Last week’s PCE data showed headline inflation remaining elevated at 4.1% (with core PCE registering 3.4%), in line with the central bank’s updated Summary of Economic Projections, which sharply raised the median year-end 2026 PCE inflation forecast to 3.6% (and core PCE forecast to 3.3%). This outlook was mirrored in a highly divided June “dot plot,” where 9 out of 18 officials projected at least one 25 basis point rate hike before December 2026 to combat these persistent price pressures, while 8 other officials projected no rate activity, and one other official projected a rate cut of 25 basis points. Because Chair Warsh has intentionally adopted a shorter, less predictable communication strategy, the upcoming rate decisions will be hyper-dependent on incoming data.

Best wishes to all for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 6/26/26. GDP, PCE, and Personal Income and Outlays are sourced from the U.S. Bureau of Labor Statistics. PMI data is sourced from S&P Global Inc. Weekly Jobless Claims are sourced from the U.S. Department of Labor. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.