Resilient Labor Market and Lingering Inflation Delay Rate-Cut Hopes

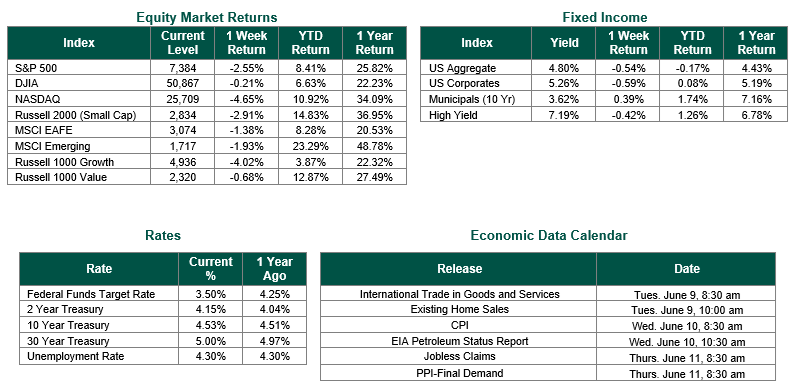

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index closed the week at a level of 7384, representing a decrease of -2.55%, while the Russell Midcap Index moved -1.17% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -2.91% over the week. As developed international equity performance and emerging markets were negative, returning -1.38% and -1.93%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.53%.

Last week, U.S. employment data came in mostly stronger than expected, led by the May Employment Situation report, which showed nonfarm payrolls rising by 172,000 versus consensus around 80,000–95,000 and up from an upwardly revised 179,000 in April, while unemployment stayed at 4.3%, exactly as expected. U.S. Bureau of Labor Statistics (BLS) Job Openings and Labor Turnover Survey (JOLTS) report for April was released on Tuesday. The reported showed that U.S. job openings surged by 731,000 to reach 7.6 million, marking a near two-year high that easily defied consensus expectations and shattered the previous month’s revised baseline of 6.9 million. While this headline number points to unexpectedly robust labor demand, a look beneath the surface reveals a highly bifurcated “low-hire, low-fire” environment. Actual hiring declined significantly by 419,000 to 5.12 million, and the overall quits rate dipped to 1.9%, reaching its lowest level since 2020 and signalling that workers are increasingly hesitant to leave their current roles. Layoffs also edged down slightly to 1.7 million, proving that while firms are keeping their current staff, they are pulling back on onboarding new employees. The ADP private payroll report also beat expectations, with 122,000 jobs added in May versus a 110,000-consensus forecast and a much weaker prior pace implied by the market’s pre-release setup, reinforcing the view that labor demand remained resilient.

The broader message from the week was that the labor market was still firm rather than cooling sharply, with payroll gains spread across leisure and hospitality, health care, and government, and wage growth holding steady enough to support household income without signaling acute labor slack. The unemployment rate’s stability at 4.3% and the slightly improved broader underemployment measure added to the sense that conditions were steady rather than deteriorating. The market interpreted that as evidence that the economy could continue to grow without immediate labor-market stress.

The upside surprise in employment pushed expectations for Federal Reserve easing further out, because stronger hiring made near-term rate cuts less likely and even raised talk of a more hawkish policy path. That shift generally supported higher Treasury yields and weighed on equities even as the major averages had earlier touched record highs during the week, with investors worrying that solid labor data could delay cuts.

Friday saw a high level of volatility as the major equity indices experienced sharp selloff, driven by a combination of an overheating labor market and cooling AI infrastructure enthusiasm. The tech-heavy Nasdaq Composite cratered 4.18% (dropping 1,121.53 points to close at 25,709.43), logging its worst single-day performance since April 2025.

In short, the employment data were good for growth confidence but less helpful for near-term rate-cut hopes and risk assets, specifically tech stocks.

Best wishes to all for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 6/5/26. The Employment Situation Summary report and the JOLTS report are sourced from the U.S. Bureau of Labor Statistics. The ADP Private Payrolls data is sourced from Automatic Data Processing Inc. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.